Universal vs. Term Life Insurance: A Comparison for Canadians

TL;DR: Is term or universal life insurance better?

For most Canadians, term life insurance is the better choice.

Universal life insurance makes sense in specific situations, like estate planning, covering future taxes, or high-net-worth strategies where traditional registered accounts have already been maxed out. If this sounds like your financial situation, then lifelong coverage and tax-advantaged cash value could be a good investment.

Universal vs. term life insurance, compared

The two main differences between universal and term life insurance are how long you have insurance coverage and how much you’ll pay.

- Universal life insurance lasts your whole life. It accumulates cash value that you can use, but premium payments are a lot higher. It includes more risk and it’s more complex to manage.

- Term life insurance covers you for a set term, usually 10, 20, or 30 years. It’s cheaper than universal coverage, and the money you save can be invested elsewhere to save for your financial future.

“I don’t always recommend life insurance as an investment. But for a higher-net-worth client, we will often use life insurance as a savings mechanism for funds they wouldn’t otherwise use while living.” – Susan Cruikshank, Senior Tax Manager at BDO Canada LLP

Coverage duration

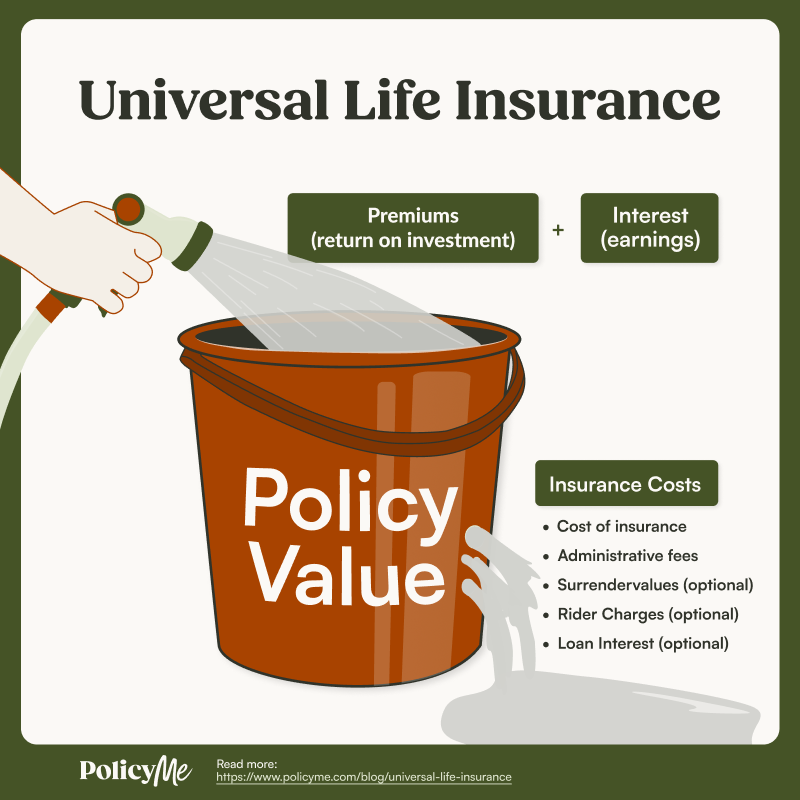

Universal life insurance covers you for your entire life, as long as you keep the policy funded.

- You pay premiums for life (at a higher rate)

- Your beneficiaries get a payout no matter when you pass away

Term life insurance covers you for a set number of years (aka, your term) and then expires. At this time, you can usually renew (at a higher cost, since you’re older) or purchase a new policy.

- Your premiums end when your term ends

- Your coverage ends when your term ends

- Your loved ones get a payout only if you die during the term

The bottom line: Term is a better choice to protect your family while you’re paying off a mortgage, raising kids, or covering other financial responsibilities. Universal may be better if you have specialty estate considerations or need lifelong coverage.

Premiums

Universal life insurance premiums are generally higher. This type of permanent life insurance can also be adjusted within certain limits, but you need to actively manage your policy to keep it funded.

Term life insurance premiums are generally lower. They’re also fixed for the length of your term, making it the more budget-friendly and predictable choice. The coverage amount and specific period of time will impact your premium, too.

Cash value or savings component

Universal life insurance policies do build a tax-deferred cash value. You can borrow against the policy’s cash value or withdraw, but this might reduce your death benefit if you don’t pay back the policy loan.

Term policies do not have a cash value or savings component. If you’re still alive when the term ends, there is no payout or cash reserve.

The bottom line: For most Canadians, the cash accrual feature of universal life insurance is actually less helpful than investing for retirement planning or setting aside cash in a high-yield savings account.

“If you buy an expensive permanent insurance plan, it’s going to take money away from saving for a down payment, which might be more important. Maybe instead, you consider a cheaper term insurance policy that will get you what you want from an insurance perspective without jeopardizing savings for retirement, for a house, or whatever it may be.” – Erik Heidebrecht, Licensed Insurance Advisor

Simplicity

Universal life insurance policies have more components and take active effort to maintain.

- Requires knowledge in investment/finance

- Requires time to manage the policies successfully

- Requires management for the entire duration (aka your lifetime)

Term life insurance policies require no management once you’ve purchased a policy.

- Offers various term length and coverage options

- Requires you only to pay your premiums every month

- Has the ability to renew or convert to permanent coverage at the end of the term

The bottom line: A universal life policy might be a good fit if you have the skill (and time) to manage it, or if your family has complex estate planning needs. But for most Canadians, term life insurance offers the right amount of protection with no day-to-day involvement.

Read more: The best term life insurance in Canada

Types of universal vs. term life insurance

Universal and term life insurance are two types of insurance, but they fit into a bigger world of life insurance. The two main categories of life insurance are permanent (lifelong) and term (temporary) — universal is one type of permanent coverage.

Permanent coverage is lifelong, and includes these types:

- Whole life insurance: Cash value, level premiums, possibly dividends (participating vs. non-participating)

- Universal life insurance: Cash value, flexible premiums.

- Term to 100: Level premiums till age 100, no cash value.

Within universal life insurance, there are three types of UL:

- Guaranteed universal life insurance (GUL): Little or no cash value growth

- Indexed universal life insurance (IUL): Cash value tied to stock market index

- Variable universal life insurance (VUL): Cash value depends on your choice of investment account options

Term coverage is temporary, based on a term length you select (between 5 to 40 years). Term policies may be renewable (get a new term policy) or convertible (convert term to permanent).

No, permanent is the overarching category for lifelong coverage. Universal and whole policies are two types of permanent coverage that differ in flexibility, stability, and policyholder involvement.

Universal vs. term: which one should you choose?

Term is best for most Canadians (and it’s also the cheaper of the two!). The only Canadians who should be considering universal coverage either have lifelong dependents or specific estate planning concerns.

You can always speak with an advisor if you want the peace of mind that comes with speaking to an expert.

Is term life insurance better than universal life insurance?

For most Canadians, term life insurance is better than universal life insurance. It has more advantages for you and your loved ones.

- Premiums are more cost-effective due to underwriting

- Fixed premiums

- Coverage better aligns with financial obligations

- Policies may be personalized

- Set-and-forget protection

When does universal life insurance make sense?

Universal life insurance may make sense if you:

- Have already maxed out traditional savings and investment avenues

- Have permanent dependents or other financial obligations, such as a disabled child

- Are a high-income household or have other complex estate planning needs

Universal life insurance usually does NOT make sense if you:

- Just want affordable coverage to protect your family while you’re working

- Do not want market risk or investment complexity as part of your life insurance

- Have not yet maxed out your TFSA or RRSP yet

FAQ: Universal vs. term life insurance

Bonnie Stinson is an insurance writer and researcher in Toronto with a decade of experience producing helpful, accurate content for Canadians. They have published resources for some of Canada's most innovative and consumer-trusted companies in the health, legal, and fintech sectors.

Bonnie Stinson is an insurance writer and researcher in Toronto with a decade of experience producing helpful, accurate content for Canadians. They have published resources for some of Canada's most innovative and consumer-trusted companies in the health, legal, and fintech sectors.