Is Life Insurance Worth It? Yes, for Some People

Is life insurance worth it?

Life insurance can be worth it if you have loved ones who rely on you financially and may struggle to pay bills or maintain their lifestyle in your absence.

A tax-free payout after your death can be a major help to your beneficiaries with any loose ends your passing might cut short, like paying off shared bills and raising kids.

Life insurance is worth it in Canada for people who have:

- Large debts, like a mortgage balance, a business loan, or significant credit card debt

- Loved ones (kids or spouse) who depend on their income and would financially struggle without it

- Financial goals that would be impeded by premature death

If you don’t have many projects on the go or you’ve undertaken sound financial planning, life insurance may not be as important. But different types of life insurance can still provide the means for post-life goals such as inheritances, funeral expenses, estate planning, or charitable donations.

As a rule of thumb, term life insurance is generally worthwhile for the average Canadian's financial needs.

According to the PolicyMe 2025 Life Insurance Gap Report, 1 in 4 Canadians (25%) is not confident or is unsure that their families would be financially secure if they passed away unexpectedly.

Who needs life insurance?

Life insurance can be helpful in Canada for people with dependents, shared debts, or who want to leave a guaranteed legacy and haven’t yet saved enough to do so.

Here are a few of the key demographics who do need life insurance:

- Parents: Life insurance is an essential financial safety net for your children. It can also help to cover childcare costs, education, and even extracurriculars after you’re gone, especially if you’re a single parent.

- Homeowners: If you have an active mortgage, life insurance ensures that your debt won’t become an unmanageable burden to your loved ones if you pass away before it’s paid off.

- Business owners: Running a business comes with ongoing costs. Life insurance can make sure they’re paid even after you’re gone.

- Early career adults: If you’re building a career that promises high earnings in the future, buying life insurance at an early stage can help you lock in low rates on major protection.

- Seniors: As you’re approaching end-of-life decisions, a life insurance policy can help you leave behind financial support for your loved ones to cover final expenses including burial.

Who doesn’t need life insurance?

If you do not have dependents, large debts, or post-life goals (or you already have enough savings to cover them), then you may not need life insurance or a life insurance payout.

However, life insurance options are flexible and can be worth it at any age — the key is to think about your responsibilities and financial situation and pick a policy that fits your needs.

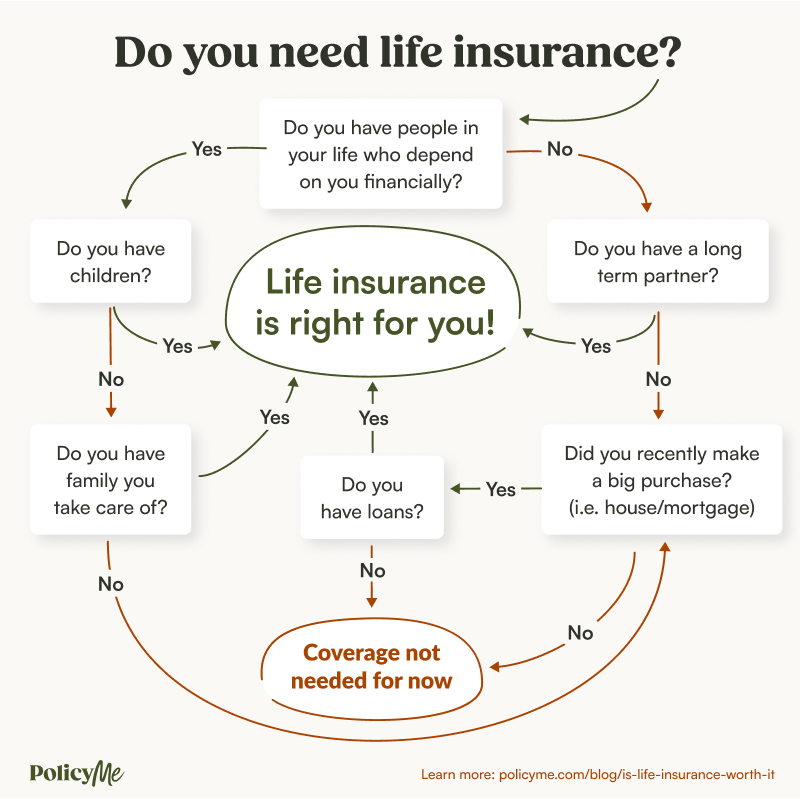

Do I need life insurance?

The simplest way to decide if you need life insurance is to think about the three why’s of life insurance: dependents, debts, and post-life goals:

- Dependents: Does anyone rely on me and my income for current or future stability?

- Debts: Do I have any shared debts that would be a burden on my loved ones if I died?

- Post-life goals: Could I comfortably cover my final expenses or leave an inheritance if I died tomorrow?

Start with the image below.

For most families, the loved ones left behind after a premature death may struggle to take care of themselves financially.

Even if you understand that life insurance is valuable, you may still wonder, is it worth it? Or rather, what kind of life insurance policy is actually worth it for me? How much coverage do I need? Do I buy now or wait?

Reflect on these questions by yourself or discuss them with your partner:

- How many people rely on me financially? Don’t just think about legal dependents like children. Your partner, parents, or other family members might depend on your income in full or in part—or you may expect them to become dependent in the future.

- What’s my total debt, and is it shared? When you die, your outstanding debts will pass to your estate. If your assets (e.g., property, savings, and investments) aren’t enough to cover them, they could pass to anyone who shared the debt, such as a spouse or a family member who co-signed a loan.

- Could my family afford a funeral right now? Death is expensive, and so is what follows. The average cost of a burial in Canada is between $5,000 and $25,000 in Canada, while cremation costs $2,000 to $5,000.

- What financial goals am I saving for? If you’re saving up for major life plans, such as your children’s college education, keep in mind that your savings could be cut short if you died unexpectedly.

- Do I want to leave a legacy? You can leave your mark in other ways, but if you’d like to leave a sizable financial gift to your loved ones, a charitable cause, or another individual or organization, life insurance is a natural mechanism for that gift.

- How much room is in my budget? For most healthy, non-smoking adults aged 30–44, term life insurance premiums are well under $50/month—and many people pay far less. If you can fit that payment into your monthly budget, life insurance may be worth it.

Why term life insurance is often enough for most Canadians

Term life insurance ($20 to $30/month) is the best type of life insurance for most Canadians if you have any financial obligations and goals that require a life insurance policy.

Term policies do not last forever, and that’s why they are so good!

- Customizable: Choose a term length that fits the length of your financial needs (5 to 40 years)

- Temporary: Coverage lasts as long as you need it and then coverage (and premiums) stop.

- Affordable: Premiums start between $20 to $30/month for $500,000 in coverage.

- Balanced: Low cost coverage now means you can invest more in long-term wealth growth.

In other words, term policies protect your loved ones during your most vulnerable years without taking a huge chunk out of your budget. You get exactly the protection you need, with flexibility in the budget for investing now and saving money in the future once your policy ends.

Here’s a look at sample starting term life insurance premiums from PolicyMe for a healthy 35-year-old with $500,000 in coverage:

* Rates current as of February 2026.

The more coverage you want, the longer the term, and the older you are, the more you’ll pay. 20-year term coverage is the most common length in Canada, as it aligns with child-rearing years and mortgage timelines.

Did you know? Many term policies are renewable and convertible. You can renew your coverage at the end of the set period if you find you still need coverage, or you can convert to a permanent policy with no medical exam if your needs change.

Why permanent life insurance isn’t worth it for most people

The higher premiums of permanent policies make it difficult to invest for the future, and this is a major reason why permanent coverage is not worth it for most Canadians.

Permanent life insurance ($260 to $340/month) includes whole life insurance and universal life insurance:

- Lifelong coverage

- Guaranteed payout for your loved ones

- Premiums are very high

- You pay those premiums forever

Here are sample starting premiums for permanent whole life coverage at $500,000 for a healthy 35-year-old applicant:

* Rates current as of February 2026.

“Many Canadians seem to believe they need permanent life insurance, but the reality is that permanent life insurance is a very specialized product that only meets the needs of a small percentage of the population.” —Andrew Ostro, Co-Founder & CEO of PolicyMe

Lifelong coverage: It sounds nice, but you probably do not need life insurance forever. Once your major debts are paid off, you’ve saved for retirement, and your dependents are no longer relying on you financially, that money could be better allocated.

Guaranteed payout: A big payment for your loved ones is a nice gift, but there are smarter ways to leave an inheritance. Permanent life insurance policies do include investment features that offer tax-advantaged growth. However, traditional savings and investment options have much higher growth rates than permanent policies.

High premiums for life: You do not get back all the money you put into cash value policies. While you can borrow against these policies, these are loans you have to repay otherwise they eat into your death benefit. Plus, insurance companies keep the accumulated cash value when you die and your loved ones only receive the lump-sum payout.

Most Canadian households simply cannot afford to pay for permanent coverage and invest for the future. It’s usually a better move to buy term coverage and then invest the rest in higher-growth options like TFSAs and RRSPs.

“Buy term and invest the rest. Cover yourself when you need it most, and at the end of your term, you can reassess your coverage needs.” —Stephanie Roux, Life Insurance Advisor

If you’ve already maxed out traditional savings and investment options like TFSAs and RRSPs and want to supplement your retirement income, permanent coverage or a whole life insurance policy may be an option. But unless you have a high net worth, lifelong dependents, or complex estate planning needs, a term life insurance policy with lower premiums and targeted coverage is likely the most cost-effective life insurance option.

Not sure what type of policy you need or how much coverage to buy? PolicyMe’s free online life insurance calculator is a quick way to evaluate your life insurance needs based on your annual income, mortgage payments, retirement savings, family structure, and more.

Ask an expert: do I need life insurance?

If you’re not sure whether you need life insurance, it can help to hear from an expert. Licensed life insurance advisor Stephanie Roux shares the recommendations she made to four real-life Canadian couples and individuals facing the same question.

Elena and Feng from Burnaby, BC

Elena (31) and Feng (33) have been married for two years and hold a $500,000 mortgage together. Elena works as a financial controller, while Feng is a coordinator at a non-profit.

Is life insurance worth it for Elena and Feng?

"Elena and Feng need life insurance. If one of them were to pass, the surviving spouse would have to cover the mortgage. And without their partner's income, the other might need help with daily expenses. That's why death benefits from a life insurance policy are so critical."

Asma from Calgary, AB

Asma (33) is a business analyst who owns a condo and has a mortgage with $250,000 remaining. Although she makes all the payments herself, her mother was a co-signer.

Is life insurance worth it for Asma?

"Asma needs life insurance. She has a mortgage that needs to be paid if she passes. And because her mother has co-signed, she'd be responsible for the payments. Any other outstanding debts she has could also become her mother's responsibility. She doesn't want to burden her with these costs. That's why life insurance is important."

Laila from Regina, SK

Laila (24) is a student and only a few months away from completing her studies. To keep costs low, she attends an affordable program and lives with her working parents, who can comfortably provide for their own needs.

Is life insurance worth it for Laila?

"Laila probably doesn’t need life insurance. She has no debts or dependents."

Barb and John from Barrie, ON

Barb (58) and John (62) have grown children who just moved out. The two of them are still working to pay off their shared mortgage before retiring for good.

Is life insurance worth it for Barb and John?

"Barb and John need life insurance. They still have an outstanding balance on their mortgage. Financially, their children are just starting out and may not have the money to support the surviving parent."

Next steps

If you choose to buy life insurance: Make sure that you understand the pros and cons of term vs. whole life insurance, as well as the strengths of individual life insurance companies. Once you’ve settled on the right coverage, request life insurance quotes from a few companies to compare your eligible rates.

If you choose not to buy life insurance: If you don’t need life insurance right now, be prepared to revisit this question after any major life changes, such as the purchase of a property or the birth of a child.

FAQ: Is life insurance worth it in Canada?

You need facts, not fluff. Our goal is to provide you with honest, trustworthy information to help you make informed decisions. While our content is created with insurance experts, it is for educational purposes only and should not be considered definitive professional financial advice. We recommend seeking the counsel of a licensed financial professional before making any decisions regarding insurance or personal finance.

Bonnie Stinson is an insurance writer and researcher in Toronto with a decade of experience producing helpful, accurate content for Canadians. They have published resources for some of Canada's most innovative and consumer-trusted companies in the health, legal, and fintech sectors.

Bonnie Stinson is an insurance writer and researcher in Toronto with a decade of experience producing helpful, accurate content for Canadians. They have published resources for some of Canada's most innovative and consumer-trusted companies in the health, legal, and fintech sectors.