6 Advantages of Term Life Insurance in Canada

The advantages of term life insurance

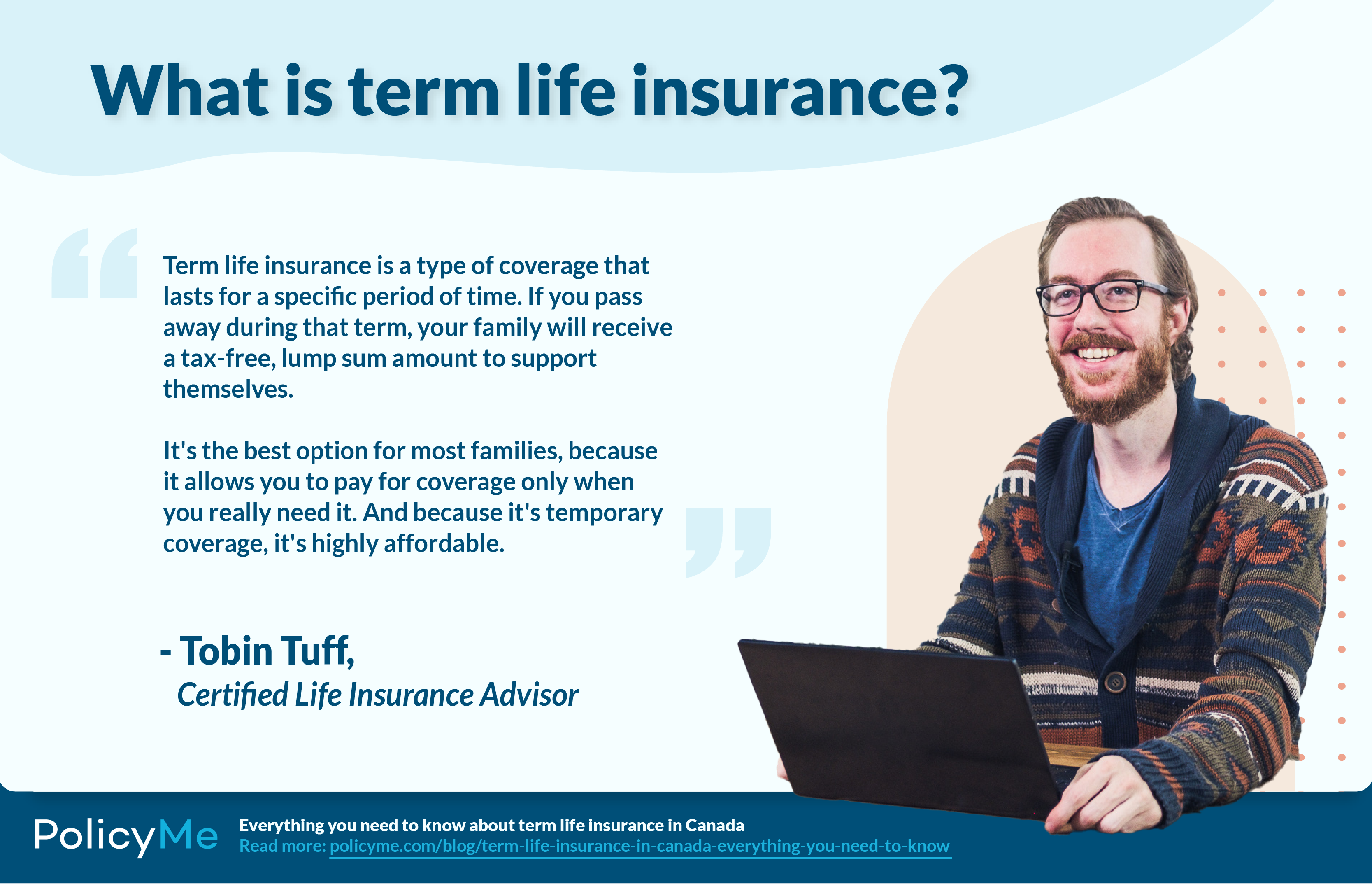

Term life insurance is one of the most practical and affordable ways to protect your family. It’s designed to provide coverage when you need it most, without locking you into expensive lifelong payments.

Here are some of the benefits of term life insurance vs. a lifelong permanent life insurance policy.

1. It has affordable monthly premiums

Generally speaking, term coverage is the most affordable type of life insurance for most people. Premiums stay consistent for the entire term, and locking in a low rate while you’re young and healthy can make coverage especially cost-effective. It’s a simple, budget-friendly way to ensure your loved ones are financially protected during the years they need it most.

2. It locks in your rates

With term life insurance, your monthly premiums stay level for the duration of your term, making it easy to budget over the long term. The earlier you get coverage, the better. Young, healthy people enjoy the lowest life insurance rates, securing affordable protection that will follow you through milestones like raising a family, building a career, and paying off a mortgage.

3. It allows you to pay only for what you need, when you need it

The average Canadian doesn’t require life insurance for a lifetime. Term insurance allows you to choose how much coverage you need and for how long—for example, a 30-year term might cover you while your kids are growing up and you’re paying off your mortgage. Once those financial obligations end, you can allow your coverage to lapse (or consider other options).

You can also “stack” or “ladder” term policies of varying lengths to cover specific needs. For example, if you have 20 years left on your mortgage but your kids will be financially independent in 10 years, you could stack a 20-year term policy to cover your mortgage and a 10-year term policy to protect your dependents. This approach helps you match coverage to your changing financial needs and avoid paying for more insurance than you need

4. It (often) offers convertible options

If you still need coverage when your term ends, you may have the option to renew it or purchase a new term. Alternatively, many term policies allow you to convert to permanent coverage without undergoing a new medical exam.

5. It’s flexible for every stage of life

Whether you’re newly married, raising kids, or planning for retirement, term life coverage fits a wide range of needs. You can choose the coverage amount and term that align with your current goals, like replacing income while raising your family or protecting a new mortgage. As your life (and financial situation) changes, you can adjust your coverage to ensure you’re not overpaying for protection you don’t need.

6. It’s simple and easy to understand

Permanent policies can be complicated, and some require active management or investment knowledge to keep them in good standing. Term coverage is straightforward—the policy pays a tax-free, lump-sum death benefit to your beneficiaries if you pass away while it’s active. It’s also low maintenance; you can get it and forget it, and have the peace of mind that your loved ones are protected.

Term life insurance offers peace of mind at a price most Canadians can afford. With predictable payments and flexible plans, you’ll always know exactly what you’re paying for and how long you’re covered.

Why term life insurance is usually the best choice

For most Canadians, term life insurance strikes the fine balance between affordability and financial protection. It’s designed to cover you during the years when your family depends on your income the most, like while paying off a mortgage or raising kids.

Permanent life insurance, on the other hand, offers lifetime coverage and a cash value component at steep prices. For many families, those extra features are unnecessary and take money away from other priorities, like education and retirement savings.

With a term policy, you can often secure a higher coverage amount for the same—or even lower—monthly premium payments compared with permanent insurance.

“Term life insurance is a simple and affordable way to protect your family’s financial future. The key is finding a policy that balances affordability with the right coverage amount.” —Christelle Arouko, Licensed Insurance Advisor

How much is term life insurance?

The rates for term life insurance will vary depending on your age, birth sex, smoking status, and more. We’ve compiled sample rates to give you an idea of what you might pay for the life insurance coverage you need. But remember, your premium might be more or less than the rates you see here due to individual factors.

Here are sample monthly rates for nonsmoking women:

And here are sample monthly premiums for nonsmoking men:

Term life vs. whole life insurance policies

Both term and whole life insurance can protect your loved ones, but they work in different ways. While most Canadians can benefit most from term life insurance, the right choice depends on your situation.

Term life insurance covers you for a set period, such as 10, 20, or 30 years. It’s designed to protect your family during your working years, when they rely on your income the most. As a result, it’s typically much more affordable than whole life insurance—and you’ll pay the lower premiums for fewer years.

Whole life is a type of permanent life insurance, and it covers you for your entire life as long as you pay the premiums. It includes a cash value component, which grows over time and may be borrowed against. Whole life coverage is usually significantly more expensive—often several times the cost of a comparable term policy.

Learn more: Term vs. whole life insurance

How to choose the right term life policy

Choosing the right term life policy comes down to factors like your budget, lifestyle, and financial goals. Here are a few things to consider before applying:

- Your age and health

- How much coverage you need, and how long you need it for

- Your budget

- Whether your lifestyle or job increases your risk level

- What’s important to you in a life insurance company

The bottom line: Term life insurance is intended to protect your family, not grow your wealth. Matching your coverage to your current and anticipated future financial commitments ensures you have enough protection without overpaying for unnecessary coverage.

FAQ

Helene Fleischer is Content Marketing Manager at PolicyMe, with 9 years in content marketing and 4 in Canada’s insurance industry. She works with skilled writers and licensed insurance advisors to create useful resources that help Canadians navigate insurance decisions with confidence and clarity.

Helene Fleischer is Content Marketing Manager at PolicyMe, with 9 years in content marketing and 4 in Canada’s insurance industry. She works with skilled writers and licensed insurance advisors to create useful resources that help Canadians navigate insurance decisions with confidence and clarity.