Critical Illness Insurance in Canada: Is it Worth the Cost?

The hidden costs of serious illness

It’s easy to assume that public healthcare and your own supplemental health insurance would cover all of your costs in the event of a major diagnosis like cancer.

Unfortunately, that’s not always the case. Canadians diagnosed with serious medical conditions often face unexpected additional expenses that aren’t covered by public or private healthcare — or by disability insurance.

Out-of-pocket costs may include:

- Prescription drugs: Depending on your existing healthcare coverage, specialty drugs may or may not be covered.

- Home care: Private or group health insurance may cover a portion of home care costs, but you may still face steep out-of-pocket costs.

- Time off work: Critical illness typically requires time away from work, from taking time to process your diagnosis to appointments and treatment. Disability insurance offers partial income replacement, but this is subject to policy terms and won’t replace your full income.

- Travel to and from appointments: A serious illness can feel like a full-time job, complete with a regular commute, which may take you out of your way if you need to see a specialist in a distant city.

- Increased daily living expenses: During a major medical crisis, daily life gets expensive. Your budget may need to accommodate food and grocery delivery, additional childcare, and home cleaning that weren’t previously necessary when you were well.

When Kim was diagnosed with a rare bone cancer, she was grateful for robust public health insurance as well as her employer’s generous group insurance plan for both health and disability coverage. But she still found herself facing nearly $40,000 in expenses related to her diagnosis that weren’t covered by insurance:

- Lost income: Between chemotherapy, radiation therapy, and surgery, Kim needed to take 12 months off her job as a bank manager. Her employer’s disability insurance only covered 75% of her $110,000 salary, which meant taking a loss of $27,500.

- Travel: Kim needed to travel two hours from home to receive five weeks of radiation therapy in Toronto. Because of the distance, she stayed in a hotel while receiving treatment. Between gas, parking, and accommodations, her travel costs amounted to $4,900.

- Childcare: While Kim already paid for daycare for her three-year-old, she needed to hire a full-time live-in nanny during her radiation treatment, which cost her around $4,500.

- Home cleaning: Kim couldn’t keep up with routine home care during her year of treatment. She hired a home cleaner on a monthly basis for a total of $2,400 over the course of the year.

- Prescription drugs: While her chemotherapy was covered by the Ontario Health Insurance Plan (OHIP), the anti-nausea medication Kim’s doctor prescribed during treatment wasn’t. Her employer’s group health insurance plan only covered 80% of the cost, leaving her with $250 in uncovered medication costs over the course of chemo.

In total, Kim paid $39,550 out of pocket for costs directly related to her diagnosis that weren’t covered by public or private insurance.

When critical illness insurance is worth it

Critical illness insurance coverage tends to be worth it if you and your loved ones would face immediate financial pressure with a serious diagnosis. For example:

- Losing income would cause financial strain

- Dependents are relying on your paycheque

- You don’t have a strong emergency fund

- Your family has a medical history of major illness

- You have limited or no disability insurance

Ask yourself: if you were unable to work for months due to illness, could you still support yourself or your family out of pocket?

No one plans to become seriously ill, but 2 in 5 Canadians will experience cancer and over 10% of hospitalizations in Canada are due to heart conditions, stroke, and vascular disorders.

When critical illness insurance may not be worth it

Critical illness insurance is not for everyone. You probably don’t need CI coverage if:

If you don’t yet have a financial safety net, your money may be better directed toward building an emergency fund or paying down debt. Once your finances are more stable and you can comfortably manage a monthly premium, you can revisit critical illness insurance.

How critical illness insurance works

Critical illness insurance offers a lump-sum payment while you’re alive if you are diagnosed with a covered critical illness. This type of coverage is designed to be a financial buffer, giving you quick access to cash if you’re experiencing serious health issues.

Critical illness insurance can be either term coverage for a set period or permanent coverage for life.

You may be asked questions about hereditary conditions or past illnesses in your application. Like other forms of insurance, you must pay a monthly insurance premium to keep your policy active, but you’re free to spend the money as needed.

What’s typically covered? Cancer, heart attack, stroke are commonly covered. You must meet your policy’s definition of a “serious condition” and only listed conditions are covered.

Critical illness waiting periods and survival requirements

Critical illness insurance plans are subject to specific restrictions based on the date of diagnosis and type of illness you’re facing.

In most cases, a waiting period of at least 30 days after diagnosis applies to your coverage. However, that waiting period could be shorter or longer depending on the details of your diagnosis:

- Conditions with no waiting period may include blindness, deafness, and aplastic anemia (bone marrow failure).

- Conditions with a 30-day waiting period may include many major surgeries, cancers, stroke, and heart disease.

- Conditions with a 90-day waiting period may include bacterial meningitis, paralysis, and occupational HIV infection.

In order to qualify for coverage, most critical conditions must be diagnosed by a specialist. You may also be required to demonstrate that symptoms have been ongoing for a certain period of time in order to file a claim.

What critical illness insurance typically covers

A typical critical illness insurance policy in Canada will cover around 20 serious conditions, such as stroke, cancer, organ failure, paralysis, loss of limb, multiple sclerosis, severe neurological conditions (ALS, advanced Parkinson’s), and heart attacks.

Read your policy carefully; each insurance provider covers different illnesses and has different qualifiers and exclusions.

These insurance companies cover the most critical illness conditions in Canada:

- PolicyMe: 44 conditions

- Sun Life: 34 conditions

- RBC: 32 conditions

- Manulife: 31 conditions

- BMO: 29 conditions

On the other end of the spectrum, you can find very basic critical illness insurance products that only cover about five illnesses.

Be aware that some plans offer enhanced cancer or cardiovascular coverage. Some also offer a partial payout for “early-diagnosis” conditions—illnesses where full recovery is likely if it’s caught at an early stage.

How much does critical illness insurance cost?

The cost of critical illness insurance in Canada is between $25 and $100 per month for $25,000 and $100,000 in coverage. Prices vary depending on age, sex, health, and the provider:

- Age: Younger people pay less than older people for CI insurance because they’re less likely to suffer from a serious illness.

- Sex: Men and women are vulnerable to different illnesses at different ages, which is reflected in premium costs.

- Health: Being a smoker, having high BMI, alcohol use, and a history of illness all raise your risk of becoming ill, which means you’ll pay higher premiums. You must disclose any history of family illness and past diagnoses to get accurate underwriting.

- Provider/policy: You’ll pay more if you want a larger payout or prefer a longer term length. You’ll pay less for a shorter policy that covers fewer illnesses. If you choose to bundle with another type of insurance, like term life insurance, you might get a discount on both policies.

Even plans with similar coverage at different insurers could come with significantly different monthly premiums. Shop around with at least three companies to find a good rate.

Critical illness insurance vs. disability insurance

Both critical illness insurance and disability insurance offer financial protection if your health suddenly changes, but the payout structure differs.

Some conditions may be covered under both insurance plans. For example, critical illness insurance would pay a lump-sum benefit that you could use to cover medical bills, home modifications, or short-term income replacement while you recover. Disability insurance would replace your income while you’re unable to work up to a certain percentage of your salary.

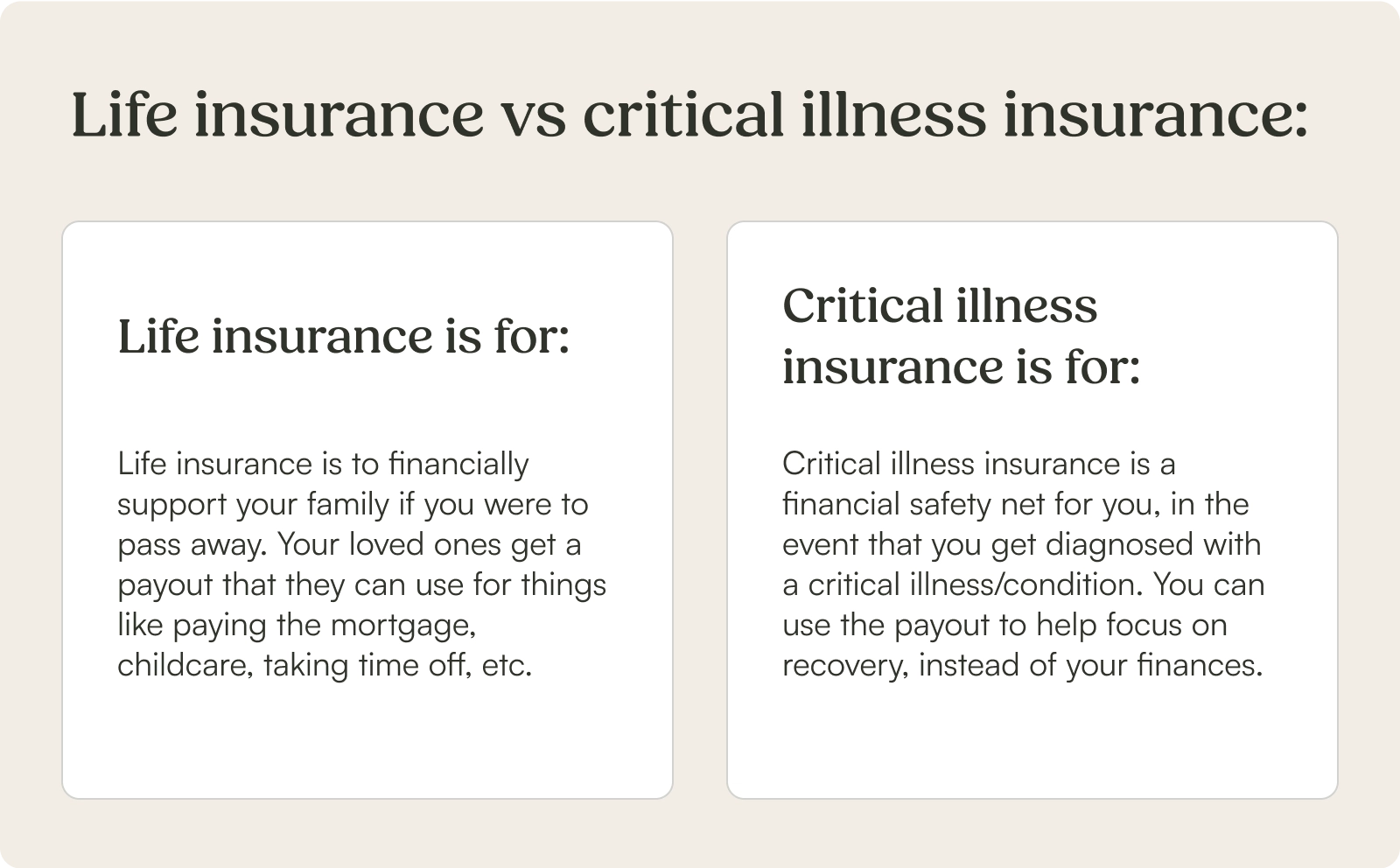

Critical illness insurance vs. life insurance

Both critical illness insurance and life insurance offer financial protection and are structured similarly; however, the intended recipient, amount of coverage, and the time of payout differ.

Critical illness is about immediate financial support if you become ill — perfect if you don’t have a big emergency fund. Life insurance is about long-term stability for the loved ones you leave behind when you pass who relied on your income.

In other words, CI pays you while you’re alive and dealing with a covered illness whereas life insurance pays your beneficiaries after your death. Both can work together to provide a complete safety net, but you should start with the one that addresses your most pressing financial concerns.

Is critical illness insurance worth it for families?

Critical illness insurance can provide guaranteed financial security in a moment of crisis.

If you and your family would struggle with unexpected medical costs, lost income, and lifestyle adjustments if you got diagnosed with a serious condition, then you should consider CI insurance to ensure financial stability in the face of illness.

FAQ: Is critical illness insurance worth it?

Bonnie Stinson is an insurance writer and researcher in Toronto with a decade of experience producing helpful, accurate content for Canadians. They have published resources for some of Canada's most innovative and consumer-trusted companies in the health, legal, and fintech sectors.

Bonnie Stinson is an insurance writer and researcher in Toronto with a decade of experience producing helpful, accurate content for Canadians. They have published resources for some of Canada's most innovative and consumer-trusted companies in the health, legal, and fintech sectors.