Term vs Permanent Life Insurance: A Simple Comparison

What’s the difference between term life insurance vs. permanent life insurance?

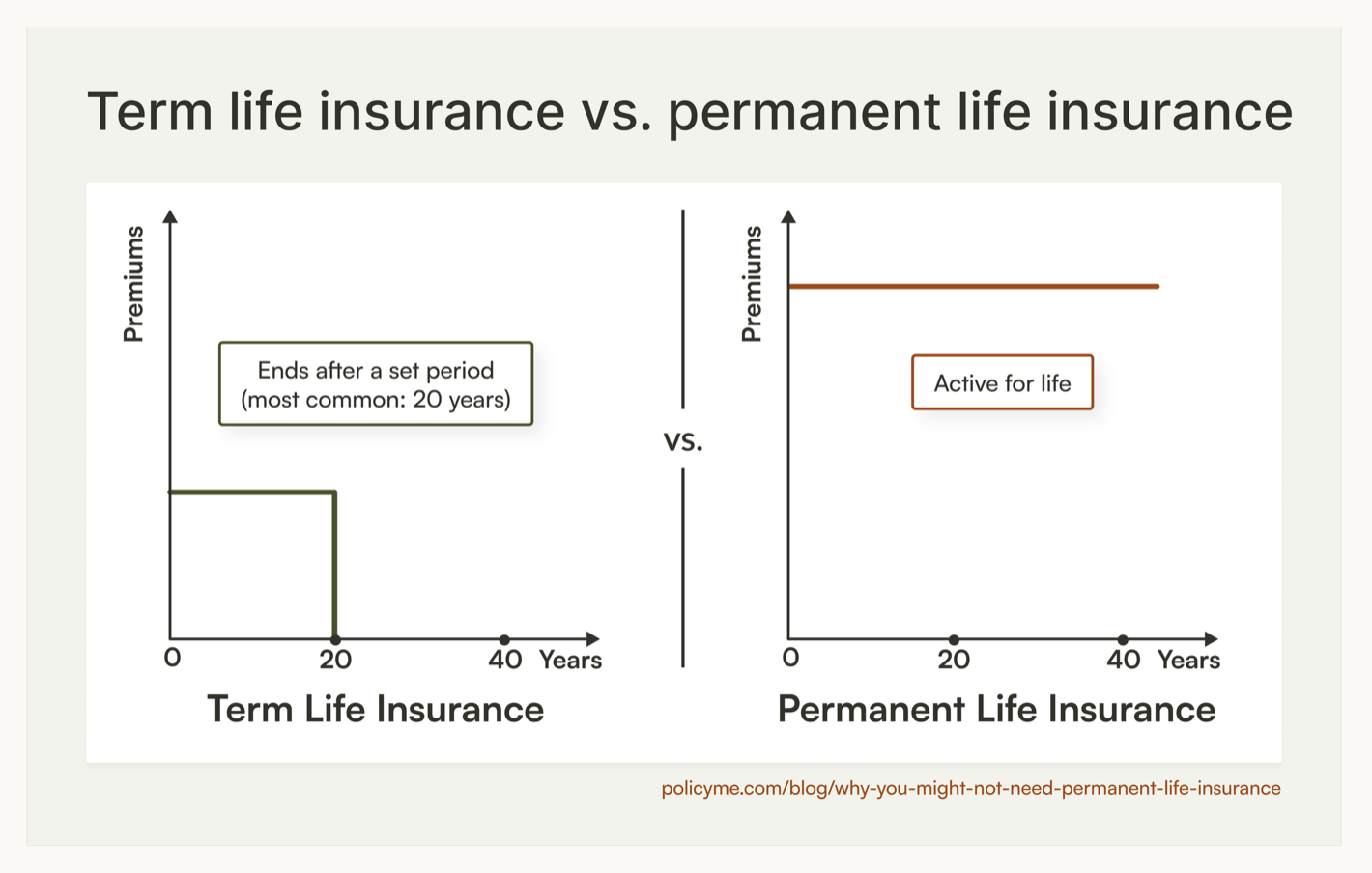

Coverage length is the main difference between these two types of life insurance policies in Canada.

- Term life insurance covers you for a set period (pays out only if you die during the term you choose).

- Permanent life insurance is lifelong (pays out whenever you die).

Furthermore, term life insurance is cheaper, more common, and a better fit for most Canadians. Permanent life insurance is very expensive, and you pay those premiums for life—that’s well past when your dependents and debts probably need you.

Term and permanent life insurance are the two main types of life insurance policies available in Canada.

The key difference between these two types of policies:

- Term life insurance pays out a tax-free death benefit to your beneficiaries if you pass away during the term’s set period.

- Permanent life insurance covers you for the rest of your life after you activate your policy, providing the death benefit to your beneficiaries regardless of when you pass away.

Term policies are becoming very popular in Canada, especially for those seeking financial protection for temporary obligations. Individual (i.e. not group) term life sales grew 40 per cent in Canada in 2021, more than double that of whole life or universal life insurance.

Let's look at each policy type further.

This quick video is a great primer:

Term vs. permanent: which one should you choose?

While most Canadians should choose term coverage, here’s a simple guide to who should get term vs. permanent:

I have a kid and a mortgage.

→ Get term: Dependents and debts won’t last forever.

I have a lifelong dependent.

→ Get permanent: They’ll be cared for no matter when you pass away.

I have a family with a history of health conditions.

→ Get term and convert: Start with term and convert to permanent with no medical exam if you develop a condition.

Scenario: Young family with a mortgage (term)

Who: Revathi (25) and Nikhil (27) chose two individual term life insurance policies. They are middle income earners with two kids.

What they’re protecting:

- Two dependent children

- Condo in Ottawa

How term coverage fits:

- One policy for each parent

- Higher payout for the higher-earning parent’s policy

- Term length aligns with children’s eventual financial independence

Scenario: High-income individual planning estate (permanent)

Who: Paulette (45) chose a permanent life insurance policy. She has no children and wants to transfer her generational wealth responsibly.

What she’s protecting:

- Inherited wealth

- Properties

How permanent coverage fits:

- Tax-advantaged $15M payout skips probate and goes directly to her niece and nephew (beneficiaries)

- Money can help pay Paulette’s final taxes without forcing property sales

Scenario: Single person with no dependents (term or none)

Who: Martin (38) chose a term policy. He is unmarried and has some retirement savings.

What he’s protecting:

- His estate

- His legacy

How term coverage fits:

- A $50k 25-year policy can cover Martin’s final expenses and estate taxes if he passes away early

- Covers a small donation to his favorite charity

Pros and cons of term life insurance vs permanent life insurance

Life insurance is a smart choice if you have financial obligations that could become burdensome to your loved ones if you pass, but the right type of life insurance policy for you will depend on your financial needs, goals, and stage of life.

Term life offers simple, affordable protection for a set number of years, while permanent life offers lifetime coverage and some financial planning advantages, but at a much higher cost.

Which is cheaper? Term vs. permanent life insurance

Term life insurance is almost always cheaper than permanent life insurance, at least for healthy average Canadians.

Take a look below at the cost comparison for the various types of life insurance policies:

* Monthly rates are based on a 30-year-old nonsmoking woman with $500,000 of coverage from PolicyMe. Men typically pay higher rates than women. Smokers pay higher rates than non-smokers.

While life insurance costs vary from person to person, there is a consistent trend when comparing term and permanent life insurance premiums. Permanent life insurance policies are typically up to 15 times more expensive than term coverage. That’s because permanent coverage is guaranteed to pay out and may include a savings or investment component.

Note that life insurance premiums vary based on age, sex assigned at birth, smoking status, health, lifestyle, coverage amount, and policy type.

Is permanent life insurance a good investment?

Permanent life insurance offers an investment component, but this doesn’t mean it’s a good investment. It can seem like a positive feature and a good selling point, but for most people, keeping investment funds in permanent policies doesn’t offer the same flexibility and potential returns that a separate investment fund would.

On top of this, the premiums on a permanent policy are significantly higher than term policy premiums, meaning you’ll have less to invest overall. If you calculate what you’ll pay for a term life insurance policy compared to a permanent one, you’ll find the difference significant.

Next, calculate what you could earn if you invested the cost difference separately, earning interest in a traditional investment account over the next 10 or 20 years.

In most cases, a term life policy is ideal to meet your family’s coverage needs and financial goals, and you can invest the difference in a separate investment account. This way you have the freedom to control how it’s invested and earn greater returns.

How do I know which type of life insurance is best for me?

The best life insurance options will depend on your specific financial responsibilities and long-term goals.

If your needs are temporary, like covering your mortgage, replacing income while your kids are still dependent, or providing financial support for a partner until retirement, term life insurance is likely the better fit. It offers affordable coverage and is designed to match the timelines of these common life stages.

Once you've decided term is right for you, calculate your coverage needs and get a recommendation for a personalized amount in about two minutes.

For those with lifelong needs, like supporting a dependent with a disability or managing a large estate, permanent life insurance products may be worth considering. Just keep in mind that the higher cost only makes sense when those needs are truly long-term.

Who is term life insurance good for?

Term life insurance is a practical, cost-effective way to protect your family during the years they need it most.

Here are some common examples:

- Parents with young children: To replace your income and cover living expenses until your kids are financially independent.

- Couples who rely on each other’s income: To help cover shared expenses while you're still working toward retirement.

- Mortgage holders: To ensure your family can pay off the home if something happens to you before the mortgage is fully paid.

- Business owners: To cover business debts or financial obligations if you're no longer around to manage them.

- Couples nearing retirement without sufficient savings: As a safeguard while building your retirement cushion.

- Those supporting elderly parents: To protect your loved ones from financial strain if you're the primary caregiver or income provider.

Who is permanent life insurance good for?

If you have permanent life insurance needs, like a disabled child or are an exceptionally high income earner, a whole life policy might make sense. Here are a few scenarios:

- High net worth individuals ($10M+ in assets): There are tax-deferred benefits for those that have already maxed out TFSA and RRSP accounts

- Canadians with complex estate planning needs: To protect the value of the estate to maximize the inheritance you pass on

- People who need a forced way to save for retirement: But this should not be a standalone retirement saving strategy

FAQ: Term vs. permanent life insurance

Bonnie Stinson is an insurance writer and researcher in Toronto with a decade of experience producing helpful, accurate content for Canadians. They have published resources for some of Canada's most innovative and consumer-trusted companies in the health, legal, and fintech sectors.

Bonnie Stinson is an insurance writer and researcher in Toronto with a decade of experience producing helpful, accurate content for Canadians. They have published resources for some of Canada's most innovative and consumer-trusted companies in the health, legal, and fintech sectors.