Best Critical Illness Insurance in Canada (2026 Review)

What is critical illness insurance?

Critical illness insurance in Canada provides a lump-sum payout if you're diagnosed with a serious medical condition covered by the policy. If your loved ones would struggle financially if you fell seriously ill and were unable to work, investing in critical illness insurance might be worth it in 2026.

Critical care insurance payouts can be used for things like:

- Paying your bills while you're off work

- Covering treatment costs and other medical expenses

- Supplementing your income

Each critical illness plan covers different medical issues. Stroke, heart attack, cancer and organ failure are covered by most (but not all!) critical illness insurance policies in Canada.

There are exclusions that apply to critical illness insurance coverage. For example, a previous cancer diagnosis or other pre-existing condition may affect your eligibility. Rules vary by insurer.

What is the most affordable critical illness insurance?

One of the cheaper CI policies on the market is offered by Manulife, with premiums that start around $35 per month. This policy only covers 31 illnesses.

The next most affordable policy is offered by PolicyMe, at around $38 per month. It covers 44 illnesses and diseases, including early-stage diagnoses.

While you can find minimalist CI coverage for $15 to $25 per month, be sure to check the fine print. These simplified plans typically only cover 3–7 core conditions like cancer and stroke, and your financial protection is often capped around $25k. This level of coverage may be enough for some Canadians, but it's worth comparing what you'd get with a more comprehensive policy before you decide.

3 things you should know about critical illness insurance

What is the best critical illness insurance in Canada in 2026?

PolicyMe takes the top spot among critical illness insurance providers in Canada due to high rankings across the categories that make a good critical illness policy:

- Payout that meets your financial needs

- Comprehensive list of conditions you’re protected against

- Affordable premiums (even more so if you combine with life insurance)

- Easy application process

Many major insurance companies offer critical care insurance products. Let’s take a look at some of the biggest names in Canada and compare their offers and covered conditions:

The insurance rates above are based on publicly available critical illness insurance quotes for a 45-year-old non-smoking woman, with $50,000 in coverage for a 10-year term as of May 2026.

PolicyMe critical illness insurance

Reviews.io score: ★★★★★ (4.82)

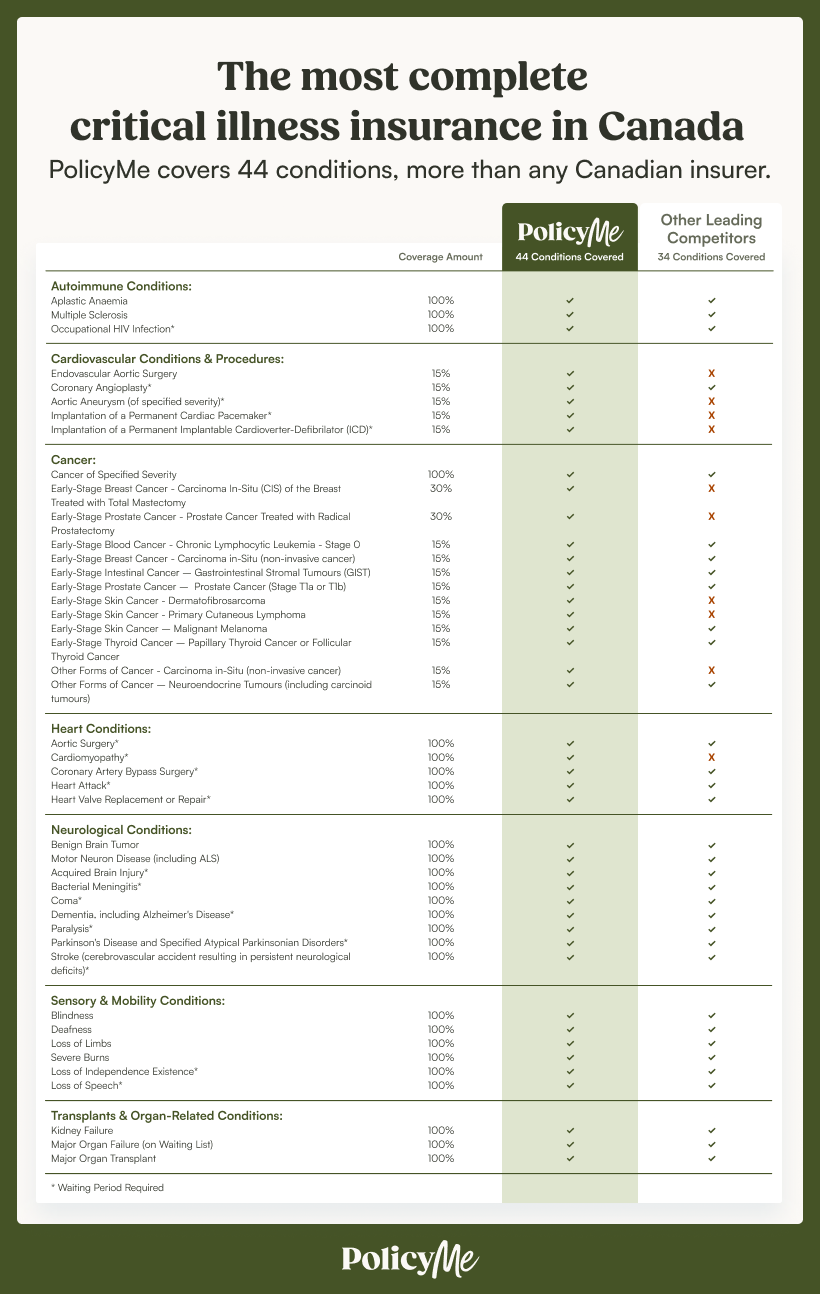

PolicyMe offers the most extensive critical illness coverage in Canada, covering 44 illnesses and conditions. Most other leading competitors in the space cover 34 or fewer. You can apply for term life and a critical illness insurance quote at the same time and receive an instant decision.

Flexible coverage options include:

- $10,000 to $1M in coverage

- 10- to 30-year term lengths (similar to our term life insurance)

- 44 covered illnesses, including more cardiovascular and cancer conditions covered than any other Canadian insurer

- No 30-day waiting period; you can submit a claim for 25 of 44 conditions after diagnosis

Sun Life critical illness insurance

Reviews.io score: ★★☆☆☆ (1.9)

Sun Life offers two types of critical care insurance plans in Canada. The less comprehensive coverage policy is called Express Critical Illness, and the more comprehensive policy is called Sun Critical Illness. You may need to speak to a Sun Life insurance advisor to learn more or apply.

- $25,000 to $3M in coverage for adults ($1M limit for child plans)

- 10-year renewable term, 75-year term, or lifetime

- 26 illnesses covered for full payout protection

- 8 less-severe illnesses covered for partial payout protection

Manulife critical illness insurance

InsurEye score: ★☆☆☆☆ (1.3)

Manulife offers three critical illness insurance plans, though the most basic critical illness benefit only covers five major illnesses. CoverMe offers online quotes, but you’ll need to speak to a Manulife advisor if you’re interested in a Lifecheque critical illness insurance quote.

Lifecheque Basic:

- $25,000 to $75,000 in coverage (limit is $50,000 for ages 56–60 and $25,000 for ages 61–65)

- 5 severe illnesses covered for full payout protection

- Optional add-on: Get eligible premiums back at age 75 if you never make a claim

Lifecheque:

- 24 critical illnesses covered for full payout protection

- 6 early intervention conditions covered for partial payout protection

- Monthly Care Benefit if you meet the criteria for functional dependence

- Optional add-on: Get eligible premiums back if you die without filing a claim

CoverMe:

- $25,000, $50,000, or $75,000 in coverage

- 5 severe illnesses covered for full payout protection

- Policy covers you until age 75, even if your health or occupation changes

BMO critical illness insurance

InsurEye score: ★☆☆☆☆ (1.0)

BMO offers two types of typical critical illness coverage: a term plan or a permanent plan with 25 covered conditions plus seven early-discovery conditions. You can also get CII as an add-on to a BMO life insurance policy.

BMO's term plan:

- $25,000 to $2M in coverage

- 10- or 20-year terms, renewable to age 75

- Convertible to a permanent Living Benefit 75 or 100 policy

BMO's permanent plan:

- Coverage to age 75 or 100

- Premiums guaranteed never to increase

How critical illness insurance works in Canada

Critical illness insurance pays out a cash benefit while you’re alive if you are diagnosed with a covered critical illness. Provincial insurance may cover some of your medical expenses but it often leaves sizable gaps in coverage that critical illness insurance can address.

You must wait for the mandatory waiting period (usually 30 days) to pass before your coverage actually begins. You can spend the payout on anything you need, from medical costs to child care.

Types of CI policies: Term or permanent

What’s covered: Serious illnesses like cancer, heart attack, and stroke are typically covered, though each company has its own list of conditions and criteria.

How to apply: You’ll need to answer health questions, choose your benefit amount, and pay the monthly premiums. PolicyMe allows you to bundle your critical illness coverage with life insurance under a single application.

How to file a claim: Before filing a claim, you’ll need an official diagnosis and must pass the survival period, if applicable (usually 10 to 30 days). If you meet the conditions of your policy, you’ll receive a payout according to your coverage details.

Who needs critical illness insurance in 2026?

Imagine you become seriously ill and are unable to work for months. Your income would decrease and your expenses would increase. If this situation would put financial strain on you and your family, you may want to consider critical illness insurance.

How much does critical illness insurance cost in Canada?

The average cost of critical illness insurance in Canada in 2026 is $25 to $100 monthly for $25,000 to $100,000 of coverage.

Higher rates are typically associated with:

- More coverage

- More covered illnesses

- Longer terms

- Older applicants

- Male applicants

- Applicants who smoke

- Applicants with previous health issues

- A family medical history of serious illness

You may pay less if you bundle CI with another type of coverage to get a discount on both policies. Do not hide your health diagnosis to get a lower rate—this could lead to a denial of payout by the provider.

Where you live in Canada generally doesn’t have a major impact on price. Small differences come down to sales tax on premiums and provincial regulation. Critical illness insurance in Ontario, for example, is similarly priced to critical illness coverage in Quebec and BC.

Get a critical illness insurance quote online in minutes.

Is critical illness insurance worth it?

Critical illness insurance is a smart purchase in 2026 if you (and your family) would face immediate financial pressure if you become seriously ill. Consider your finances and your risk tolerance.

CI insurance is designed to provide an influx of cash to support critically ill people as they deal with their condition.

Pros of CI insurance

Cons of CI insurance

One approach is to secure critical care insurance for the time in your life when a major diagnosis would hit your finances the hardest—the years when you’re paying down a mortgage or raising kids, for example.

If you already have a strong emergency fund, a gainfully employed spouse, and excellent workplace benefits, then you probably don’t need critical illness insurance.

Critical illness insurance can overlap with existing disability insurance coverage and life insurance policies. Make sure you understand the risks and benefits of each policy, knowing that you can combine multiple policies for the broadest protection.

How to bundle life and critical illness insurance

Life and critical illness insurance can be a powerful pairing. One covers your loved ones if you die and the other covers you and your household finances if you become seriously ill.

Some insurers offer a discount when you buy life and critical illness insurance together. Just make sure your policies pay out independently. With some hybrid products, a critical illness claim can reduce your life insurance benefit.

If you’re interested in bundling life and critical illness coverage, find a company that offers both policies. Shop around, pull quotes, check the fine print for covered illnesses, and make sure you’ll get a discount for bundling. Then, all you need to do is apply and pay your first premium.

Here’s how life insurance can be combined with critical illness coverage:

Choosing payout amounts: Life insurance typically replaces years of lost income for your family, while critical illness insurance covers a shorter-term financial gap during recovery. Many Canadians opt for a higher life insurance benefit relative to their CI coverage. For example: $500,000 in life insurance + $50,000 in CI coverage*. The right balance of coverage depends on your financial situation.

Choosing terms: Many people choose longer life insurance terms relative to their critical illness coverage. The logic: as you age, you're likely to have more savings and less debt, which means a serious illness later in life may be easier to financially absorb. The right terms depend on when you'd be most financially vulnerable.

So what happens if I have both policies and something happens?

- If you die, life insurance pays your loved ones. Critical illness pays nothing.

- If you get ill, critical care pays you. Life insurance pays nothing.

- If you get ill, live through the survival period, and then die, both policies pay out.

Some folks may need more critical illness coverage relative to life insurance. If you have no kids and if you’re self-employed, consider a higher immediate payout if you fear income disruption more than death-related costs.

How to get the best critical illness insurance for you

To find the right critical illness policy for your situation, ask yourself these questions:

For which conditions and illnesses do I want coverage?

- If certain conditions run in your family, start with these.

- If you don’t know, look for a company that covers a long list of diseases.

What term length fits my needs best?

- Longer policies mean higher premiums but protection for more years.

- Consider your prime earning years and how long you need protection.

What level of coverage or payout would help protect my financial security?

- More coverage means higher premiums for the duration of your policy.

- How much coverage you need depends on your personal finances.

Do customer experience and claims handling matter to me? Maybe more than price?

- Saving money is good, but not at the expense of expedient claims handling.

- Read reviews from real customers and make sure you know what to expect.

You may find that only a few companies fit your criteria after answering these questions. Then, you’re ready to request critical illness insurance quotes and potentially sign up for a policy.

Appendix: list of critical illnesses covered by PolicyMe

Here is a list of conditions covered by PolicyMe's critical illness insurance coverage:

What illnesses are covered by critical illness insurance?

PolicyMe critical illness insurance covers 44 conditions, the most in Canada. Here is a breakdown of the illnesses and conditions covered, either fully or partially:

Cancer

- Cancer of specified severity

Heart Conditions

- Aortic surgery

- Cardiomyopathy

- Coronary artery bypass surgery

- Heart attack

- Heart valve replacement or repair

Neurological Conditions

- Stroke

- Acquired brain injury

- Bacterial meningitis

- Benign brain tumor

- Coma

- Dementia, including Alzheimer's Disease

- Motor neuron disease (incl. ALS)

- Parkinson's Disease and specified atypical Parkinsonian disorders

- Paralysis

Autoimmune Conditions

- Aplastic anaemia

- Multiple sclerosis

- Occupational HIV infection

Sensory & Mobility Conditions

- Blindness

- Deafness

- Loss of limbs

- Loss of speech

- Loss of independent existence

- Severe burns

Transplants & Organ-Related Conditions

- Kidney failure

- Major organ transplant

- Major organ failure on waiting list

Cardiovascular Conditions & Procedures

- Aortic aneurysm

- Coronary angioplasty

- Endovascular aortic surgery

- Implantation of a permanent cardiac pacemaker

- Implantation of a permanent implantable cardioverter-defibrillator (ICD)

Early-Stage Blood Cancers

- Chronic lymphocytic leukemia – stage 0

Early-Stage Breast Cancer

- Breast Cancer: Ductal carcinoma in situ of the breast or lobular carcinoma in situ of the breast

Early-Stage Intestinal Cancer

- Gastrointestinal stromal tumours (GIST)

Early-Stage Prostate Cancer

- Prostate cancer – stage T1a or T1b

Early-Stage Skin Cancers

- Malignant melanoma – stage 1

- Dermatofibrosarcoma

- Primary cutaneous lymphoma

Early-Stage Thyroid Cancer

- Papillary thyroid cancer or follicular thyroid cancer – stage 1

Other Forms Of Cancer

- Neuroendocrine tumours (including carcinoid tumours)

- Carcinoma in-situ (non-invasive cancer)

Mastectomies

- Carcinoma in-situ (CIS) of the breast treated with total mastectomy

Prostatectomies

- Prostate cancer treated with radical prostatectomy

FAQ: Best critical illness insurance

Bonnie Stinson is an insurance writer and researcher in Toronto with a decade of experience producing helpful, accurate content for Canadians. They have published resources for some of Canada's most innovative and consumer-trusted companies in the health, legal, and fintech sectors.

Bonnie Stinson is an insurance writer and researcher in Toronto with a decade of experience producing helpful, accurate content for Canadians. They have published resources for some of Canada's most innovative and consumer-trusted companies in the health, legal, and fintech sectors.