Universal Life Insurance in Canada: Good Investment Strategy or Bad News?

This page provides general information about universal life insurance. Take note that PolicyMe offers term life insurance. All information provided here is for educational purposes only and should not be considered financial or legal advice.

What is universal life (UL) insurance in Canada?

Universal life insurance is a type of permanent life insurance policy that covers you for your whole life, as long as you keep paying the premiums. There are two parts to your UL insurance premiums: some of the payment goes towards the life insurance, and the remainder is divided between savings and investment components.

TikTok may have convinced you that universal life insurance is a good investment strategy and a “cheat code” for the wealthy—but this isn’t always the case. Universal life insurance policies can be confusing to understand and buy, and they’re generally not the right choice for most Canadians.

Universal life insurance is easy to customize, but you need to monitor the policy to ensure your investments are performing well and make adjustments if they’re not. Underperforming investments over the long term could result in increases to your insurance premiums—and if you can’t afford them, the policy will expire.

Almost 88% of universal life policies never pay out due to policy lapses.

How does universal life insurance work in Canada?

Universal life insurance policies offer lifelong coverage in exchange for monthly premiums. This type of policy has some unique features:

- Cash value. Over time, universal life policies gain value that you can eventually borrow against. The policies include a guaranteed minimum interest rate, but investment performance is variable and needs to be closely managed.

- Adjustable premiums. You can always just pay your minimum premium—but if you choose to pay more, the additional funds help build up the policy’s cash value. You may be able to pay less than the minimum too, but if you don’t have sufficient cash value built up to cover the cost of the policy, it will lapse.

- Guaranteed death benefit. With universal policies, the death benefit is guaranteed to be paid out when you die as long as the policy remains active. You may be able to decrease the death benefit as your financial obligations change.

There’s no doubt about it: universal life insurance is a lot more complicated than a simple term life insurance policy. It has its own benefits and drawbacks to consider.

Pros and cons of universal life insurance

Here’s a quick look at the pros and cons of universal life insurance:

Pros of universal life insurance

1. Lifetime coverage. As a type of permanent insurance, your universal life insurance policy will remain active as long as you pay your premiums.

2. Flexible premium payments. Typically, you can make adjustments to the coverage amount and premium payments over time, offering flexibility as your life or income changes.

3. Cash value accumulation. As you pay your premiums, a portion of the money goes into an account that represents the cash value of your policy and earns interest over time.

4. Tax deferral benefits. As with most life insurance policies, the death benefit paid out to your beneficiaries is tax-free. The interest earned on the cash value portion of your policy is tax-deferred, which means you won’t pay tax on the growth unless you access it during the life of the policy.

5. Variety of investment strategies. There are different types of universal life insurance, and these options give you some flexibility in choosing how the investment portion of your policy is used.

Cons of universal life insurance

1. Expensive premiums. Universal life insurance isn’t an affordable choice for most people. It can be prohibitively expensive, making it hard for policyholders to keep up payments to maintain an active policy. In contrast, PolicyMe's term life insurance rates are some of the most affordable in Canada.

2. Limited cash value. Your life insurance company may cap your cash value returns or how much you can invest based on tax laws, so ask about things like the “participation rate” or contribution limits before signing up.

3. Requires careful monitoring. There’s no hands-off version of these policies. You’ll need to monitor your policy closely to make sure you’re paying the right premiums and your cash value doesn’t get depleted. If this happens, you could lose the policy.

4. Lower returns than traditional investments. The return on the investment portion of a universal life insurance policy typically pales in comparison to what you could earn from other investments. If you really want to invest to secure your financial future, a TFSA or RRSP is probably a better option.

5. Cash value is slow to build. Cash value is an often-touted benefit of universal life insurance plans, but it takes time to build. Before you commit to a policy, be sure you understand how long it will take before you can withdraw or borrow against your life insurance in an emergency.

6. Coverage changes can trigger medical exams. While UL policies are marketed as “flexible” and adjustable over time, making changes may require a medical exam, which could lead to higher premiums.

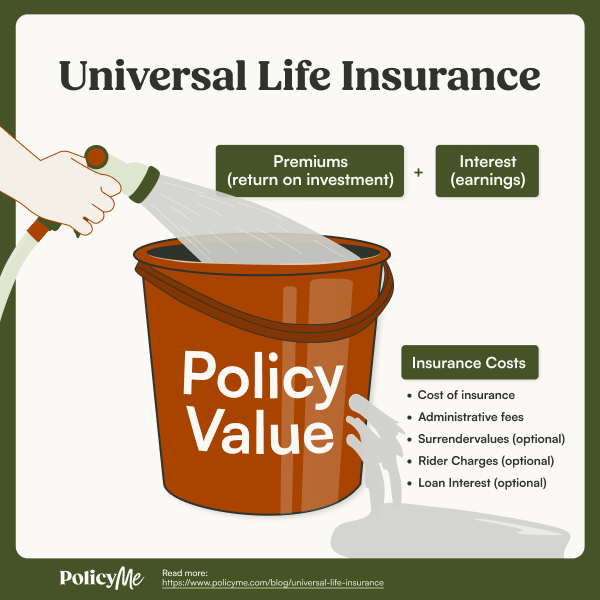

What is the cash value of universal life insurance?

Cash value is the accumulation of cash within your universal life insurance policy. This is typically what attracts people to a universal policy—but it’s more complex than you may realize.

Your universal life insurance monthly payment will include:

- Insurance cost and any admin fees

- Cash value contribution

The cash value portion of your universal insurance policy can grow over time and as your investments do well—but it can also suffer if the investments do poorly. If it does poorly over a long enough period of time, you could lose the policy altogether.

On the other hand, you may be able to borrow against the cash value of your policy. It typically takes years—even decades—to build up enough value to be able to tap into, but the option could be there if you need it.

Types of universal life insurance in Canada

There are a number of different types of universal life insurance policies. While they all offer lifelong coverage, there are differences in how they are structured.

These types of universal life insurance often have proprietary names, so you may need to do some research to make sure you know exactly what kind of policy you’re looking into.

1. Guaranteed Universal Life Insurance (GUL)

Guaranteed universal life insurance offers a universal life policy with little-to-no cash value. This is sometimes called “no-lapse-guarantee universal life insurance.” The lack of cash value means you won't have to worry about your policy lapsing because you don't have enough cash value to pay premiums.

GUL might be offered as a way to get the lowest premium payment possible on universal life coverage. At that point, the policy more closely resembles a whole life policy, so that would be a better choice.

And even more noteworthy: If you remove the cash value component, this policy ends up being even closer to a term life insurance policy. If affordability is your chief concern (rather than cash value), we recommend considering term life insurance. It will cover you for as long as you need it at a price you can afford.

2. Indexed Universal Life Insurance (IUL)

Not all insurers offer IULs—it comes down to the type of investment options they have. There are typically two:

- A fixed-rate investment account, which is lower risk

- An account tied to the performance of an index, which is higher risk

If the insurance company offers index funds, you’ll get an IUL policy—but there are lots of other investment options, including stocks, equities, bonds, and more. The returns on your investment component can be capped, which means that you may not fully participate in the gains of the underlying index.

Keep in mind: The policy fees and costs associated with index universal life insurance can be high since they include insurance premiums, administrative fees, and investment management fees. These fees can eat into the potential returns and reduce the overall performance of the policy.

3. Variable Universal Life Insurance (VUL)

Variable universal life insurance works similarly to an indexed universal life insurance policy.

Your cash value portion is invested—in this case, in investments similar to mutual funds. You'll choose how much is invested in each and based on how the funds have performed over time.

Variable universal life insurance policies tend to have higher fees and are more complex than other universal policies, and each investment fund will have management fees associated with it. It's a good idea to investigate fees carefully to ensure they don't eat up your returns.

People who prefer an active role in choosing their investment options for their policy's cash value might find these policies appealing. If you’re risk-averse or want a more hands-off approach, you might want to avoid VUL.

Does universal life insurance expire?

Universal life insurance is a type of permanent insurance, which means it’s intended to last for your entire life. As long as you keep paying your premiums, a universal life insurance policy won’t expire.

These policies typically guarantee a rate up to a certain age—and you may have to pay a significant amount to keep the policy in force if you live past that age.

If your policy lapses due to non-payment, you’ll need to start over with a new policy. Since you’ll be at a later point in life, this could be expensive. Instead, we’d recommend a more affordable term life insurance policy for seniors.

Read more: Term vs. permanent life insurance

Are universal life policies worth it in Canada?

For the average Canadian, a universal life insurance policy isn’t worth it.

While universal life is supposed to provide financial protection for your family and build wealth, these policies aren’t very effective as investment vehicles. The investment portion of universal life isn't known for strong returns, and most people are far better off using RRSPs and TFSAs, which come with tax advantages.

“Most Canadians won’t need to invest in universal life insurance—at least not until they’ve maxed out other investment options. Plus, the complexity of this type of policy makes it tricky to ensure their investment strategy will work over time.” —Erik Heidebrecht, Licensed Financial Advisor

This is where term life insurance comes in. A term policy covers you for a set amount of time—typically between 10 and 30 years. It offers more flexible protection at a fraction of the cost of a universal life policy. And since premiums are so much cheaper, you can invest the difference however you see fit.

Who is universal life insurance for?

Universal life insurance might be right for someone who wants:

- Cash value that could be withdrawn or borrowed from over the life of the policy

- Permanent coverage that lasts a lifetime

- Flexibility to adjust premiums and death benefits over time

- Control over where the investment portion is used

“Universal life insurance is for those who want to be hands-on with their policy and their investments. It’s not a set-it-and-forget-it kind of policy like term life insurance.” —Erik Heidebrecht, Licensed Financial Advisor

If we break it down further, there are two types of people for whom universal life insurance might be a good fit:

- Younger people who make a very high income, don’t need the money for decades, and can take on more risk.

- People in a high-income tax bracket who have maxed out their TFSA and RRSP contributions and want to pass down an inheritance tax-free.

Universal life insurance tends to be both expensive and complex to manage, so it's not the best choice for most people. Term life insurance is typically a better choice for Canadians who need a simple, easy-to-understand policy with affordable payments. You can invest the money you save on premiums in whatever way you see fit.

Is universal life insurance a good investment strategy?

No, universal life insurance is not a good investment strategy for most people. In most cases, you’d be better off putting your money in your RRSP or TFSA.

If you’re a high-income earner who has maxed out your other investment options, you could consider universal life as an option—but with limited returns, it’s not typically a great investment.

There are real concerns with how these policies have been sold as investments. In most cases, customers haven’t understood how the policies work and therefore haven’t monitored them as closely as needed.

The worst-case scenario: The returns are overestimated when the policies are sold, leaving people with the impression they have more financial security than they actually do. As time goes on, premiums increase, policies are underfunded, and people suddenly can’t afford to keep the policies active so they lapse.

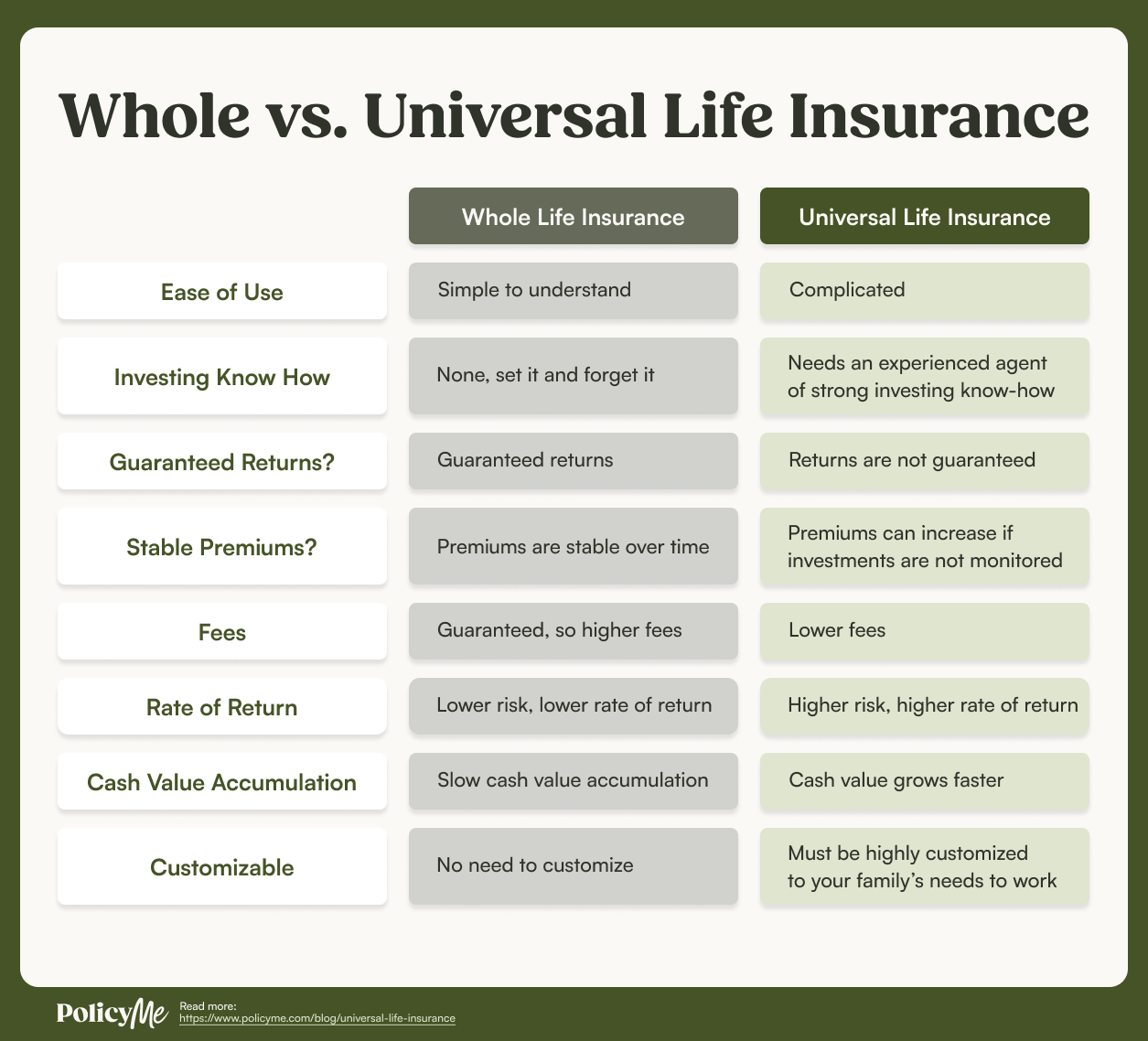

Whole vs. universal life insurance in Canada

Both universal life insurance and whole life insurance are types of permanent insurance coverage, but they differ in cost and flexibility.

Let's imagine that each of these types of insurance is a bucket to hold your money.

Whole life insurance is the safer option: You pay your set premium and the money accumulates in your bucket. Part of it goes to insurance premiums and the remainder is invested, typically into a low-risk fund with a guaranteed rate of return.

Universal life insurance has more flexibility: With universal life insurance, the amount in your bucket can fluctuate. The cost of insurance could go up and erode what you've put in, or the investments in the bucket might do poorly and your premiums could increase. If you can't pay the required premiums, your policy could lapse. You also have some flexibility in how your funds are invested, and whether you want to pay premiums monthly or annually.

Our recommendation: If you know you won’t monitor the policy to ensure you are paying the right amount over time, a whole life policy would be a better option than a universal policy. If you want to be able to make decisions about what happens to the investment portion of your policy, you may prefer the flexibility of a universal policy.

Whole vs. universal life insurance cost

Whole life insurance has a steady monthly cost that stays the same over time. While this means it may be more expensive up front, it’s stable.

Universal life insurance, on the other hand, can start out more affordably but will get more expensive as you get older.

Universal life insurance vs. term life insurance in Canada

While these are two common types of life insurance, they are strikingly different in how they work and how much they cost. Here’s a rundown of the main features of each:

Term life insurance is the smarter alternative

Term life insurance covers you for a specific period of time, such as while you have a mortgage or dependents, like underage kids or older parents. You may choose a 10- or 20-year term to ensure you are protected while this need exists.

As your financial needs decrease, so can your coverage. Very few people have coverage needs that stay level over their entire lifetimes, and term insurance gives you the flexibility to tailor your coverage to those changing needs.

Here’s an example: Let’s say you need coverage while raising a family. At the end of the term—and when you no longer have dependents to care for—you can allow your term insurance policy to expire.

You don't have to be stuck without coverage at the end of your term, either. Most term life insurance providers offer both renewable and convertible life insurance policies. That means you'll probably be able to extend your term coverage if you need to or change your policy to a permanent one down the line.

Term life insurance is far more affordable, too. This means you can likely opt for a higher death benefit while still being able to afford the payments.

The bottom line: Know the risks before committing to universal life

Universal life insurance has some appealing aspects, but also a lot of complexity—and complexity is one of the biggest pitfalls with universal life insurance. It can be difficult to assess the value of the additional components that drive up the cost of the premiums. It also requires careful monitoring that is simply beyond the knowledge (and time) of most people.

Most Canadians would benefit more from getting a life insurance quote with separate investing and savings accounts.

FAQ: Universal life insurance in Canada

Jessica is a content marketing manager with PolicyMe. She has over a decade of experience creating content, including 10 years freelancing for nonprofits and small businesses in North America and beyond. She was previously the senior editor handling car insurance content for Silicon Valley startup, and the managing editor for creditcardGenius. She's passionate about breaking down complex financial topics into clear, approachable content that helps readers feel confident about their decisions.

Jessica is a content marketing manager with PolicyMe. She has over a decade of experience creating content, including 10 years freelancing for nonprofits and small businesses in North America and beyond. She was previously the senior editor handling car insurance content for Silicon Valley startup, and the managing editor for creditcardGenius. She's passionate about breaking down complex financial topics into clear, approachable content that helps readers feel confident about their decisions.