Mortgage Life Insurance Explained: Is it Worth It?

What is mortgage life insurance?

Mortgage life insurance is an optional type of insurance policy that pays off your outstanding mortgage balance if you pass away during the amortization period. It’s usually offered by your bank or mortgage lender when you take out your loan. A mortgage life insurance policy pays the lump sum benefit directly to your bank or lender, not your family.

Here are a few key facts about mortgage life insurance:

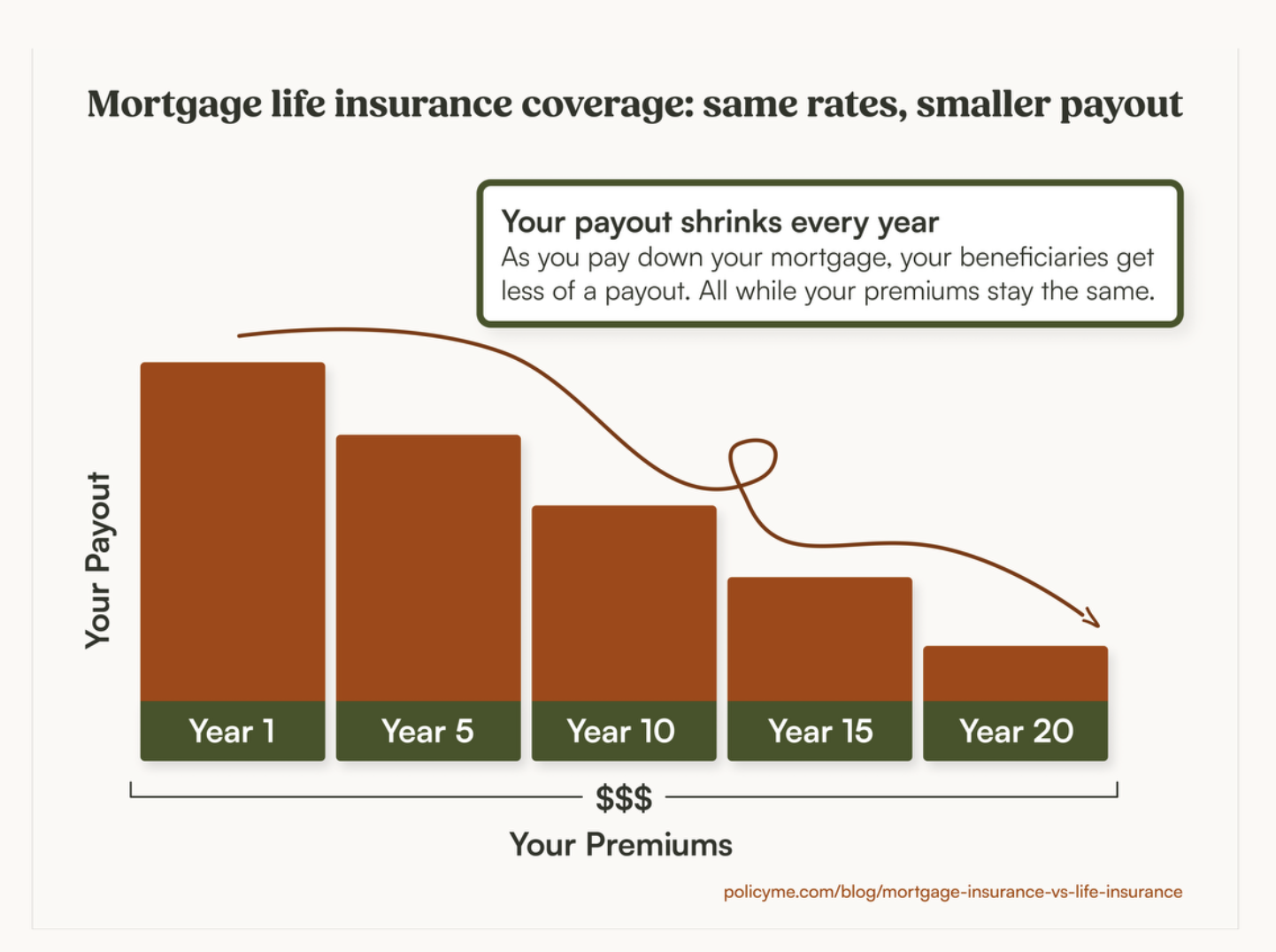

- Premiums and payout: The payout for mortgage life insurance decreases over time as your mortgage balance shrinks, but premiums stay the same.

- No portability: Coverage is tied to your specific mortgage, so if you switch lenders, move homes, or pay off your mortgage, the policy ends.

- No-medical: There is typically no medical exam required, which makes approval easier, but also means you may pay more.

- Policy type: Mortgage life insurance is not the same as mortgage default insurance, which is mandatory if your down payment is under 20% in Canada.

Is mortgage life insurance worth it?

In most cases, mortgage insurance isn’t worth it if you’re looking for broad financial protection for your family. While it helps pay off your mortgage debt directly to your lender or bank if you pass away, term life insurance is often the wiser and more flexible option to cover estate expenses and more for your family members.

Term life insurance, which is purchased through an insurance company, is typically more affordable and pays a tax-free lump sum, also called the death benefit, directly to your beneficiaries. That money can be used for anything your family needs, including mortgage payments, living expenses, debts, and final costs.

Common misconceptions about mortgage life insurance in Canada

Mortgage life insurance might sound straightforward, but there are several common myths that can lead to confusion. Here’s what many Canadian homeowners misunderstand:

Term life insurance is the better option to protect your mortgage

For dependable and comprehensive financial protection for your loved ones, term life insurance is the smarter choice. It can provide coverage for your mortgage debt and more, and it offers more control and long-term value for your beneficiaries.

Term life insurance vs. mortgage life insurance

Term life insurance is cheaper than mortgage life insurance, and it gives you more control over how your money is paid out (and can still help your dependents pay off a mortgage).

Here’s why Canadians are choosing term life insurance over mortgage life insurance:

- Payout direction: You choose your beneficiaries, so the payout goes to your family, not your mortgage lender.

- Coverage use: The payout isn’t linked to your mortgage, so it can be used for any financial need, from your mortgage to tuition or daily living expenses.

- Premium stability: Your premiums stay the same for the entire term (often 10, 20, or 30 years), unlike mortgage insurance, which can get more expensive at renewal.

- Portability: Your coverage stays with you even if you switch lenders, refinance, or move homes.

- Payout value: Your death benefit never decreases, so your family receives the full amount from the life insurance company, no matter when a claim is made during the term.

How much does mortgage life insurance cost?

Mortgage life insurance costs around $70 per month for the average applicant, compared to about $25 per month for a term life insurance policy.

You could end up paying twice as much or more for mortgage insurance premiums, even though it offers less flexibility and value.

Three main factors influence the cost of mortgage life insurance:

- Your age: The older you are when you apply, the higher your premiums.

- Your mortgage balance: The more you owe, the more you’ll pay—and premiums remain the same throughout the full duration of the policy.

- No underwriting: Mortgage insurance skips full medical underwriting, so insurers typically average pricing across all applicants, charging the same rate to both healthy and high-risk individuals.

Here’s a comparison of average starting monthly premiums for term life versus mortgage life insurance in Canada — based on a 20-year, $500K policy for a 35-year-old non-smoking woman.

The payout for mortgage life insurance policies decrease over time, but rates are fixed. Unlike with term coverage, your payout will decrease as you pay off your mortgage but your premiums will remain the same.

Why is mortgage life insurance so expensive?

The main reason it’s so pricey is that mortgage life insurance does not use full underwriting.

Without underwriting, every applicant is treated the same with regard to risk. This means that everyone pays a high price for mortgage life insurance to account for the few people who are very risky.

The other reason for the high cost of mortgage life insurance is simply that mortgages are very high right now.

Bigger loans mean higher premiums. Unfortunately, residential mortgage debt in Canada continues to trend upward, according to Statistics Canada.

Why mortgage life insurance isn’t even a last resort

When it comes to financial protection, mortgage life insurance shouldn’t be your first option. In most cases, it shouldn’t even be your Plan C.

Here’s the smartest order of operations for securing life insurance coverage for your mortgage and family:

- Plan A: Apply for term life insurance. This is the most affordable and comprehensive type of insurance coverage. Plus, if you’re healthy, it gives you the best value with guaranteed payouts for your chosen beneficiaries.

- Plan B: Try simplified issue life insurance. If you’re declined for term life, this option has fewer medical questions and no exam. Simplified life insurance premiums are typically higher, but the amount of coverage is still broader and more flexible than mortgage life insurance.

- Plan C: Consider guaranteed issue life insurance. This is for those with serious health conditions. There are no medical questions, and while coverage is limited and more expensive, it still provides more control and transparency than mortgage life insurance.

Mortgage life insurance rarely makes sense, even when your options are limited. Besides potentially paying off your mortgage if you were to pass, it offers no additional benefit to your family—and the fixed premiums aren’t typically worth the shrinking payout.

Mortgage life insurance claims are more likely to be denied

While mortgage life insurance is often marketed as “easy to get” because it doesn’t require a medical exam upfront, that simplicity comes with a hidden risk: post-claim underwriting.

Post-claim underwriting means you may not know if you’re truly covered until a claim is made. While your mortgage life insurance provider might ask a few health questions upfront, your medical history isn’t thoroughly reviewed until the claims process is initiated. At that point, the insurance company examines your records, and if they uncover something that would’ve affected your eligibility, they can deny the payout altogether.

In an interview with CBC, insurance expert Jim Bullock states, “All [policyholders] have agreed to do is pay premiums. After they die, there’s a test to see if they actually have insurance,” emphasizing that just because you have mortgage insurance, doesn’t mean you’ll qualify for a claim payout.

With a term life insurance plan, underwriting typically happens upfront, so you’ll know early on whether you’re approved and under what conditions. As long as your information is accurate and your policy is in good standing, your family can have far more confidence the claim will be paid.

“One of the selling points of mortgage life insurance is that it’s easy to get. That’s because the policy isn’t based on a health assessment or any evaluation of your individual risk,” – Laura McKay, Certified Life Insurance Advisor and COO and co-founder of PolicyMe.

Next steps if you want to cover your mortgage

Understand your current mortgage obligations, consider your dependents, and find coverage that fits your family’s financial plan.

- Confirm your mortgage details: How much do you owe? What’s the amortization period? Do you want coverage to last until the mortgage is paid off completely?

- Dependents: Would a spouse, partner, or co-borrower need help with the mortgage if you passed away? What about dependents who rely on the home?

- Review coverage options: Term life insurance coverage can fit the timeline of your mortgage. It’s often cheaper and more flexible, and the amount goes directly to your loved ones. You can cover an amount that would pay off the whole mortgage plus additional support.

- Check the fine print: If you’re seriously considering mortgage life insurance, understand portability and ownership. Will your policy stay with you even if you refinance or switch lenders?

Ultimately, the best way for most Canadians to cover a mortgage is to insure yourself with a term policy and then invest the rest to grow your wealth for the future. Mortgage life insurance is more expensive and less flexible.

FAQ: mortgage life insurance

*Life insurance rates in this article are based on publicly available premiums.

Bonnie Stinson is an insurance writer and researcher in Toronto with a decade of experience producing helpful, accurate content for Canadians. They have published resources for some of Canada's most innovative and consumer-trusted companies in the health, legal, and fintech sectors.

Bonnie Stinson is an insurance writer and researcher in Toronto with a decade of experience producing helpful, accurate content for Canadians. They have published resources for some of Canada's most innovative and consumer-trusted companies in the health, legal, and fintech sectors.