Compare home insurance quotes from top Canadian insurers

A better way to protect your home. Get real quotes from Canadian insurers in 10 minutes or less.

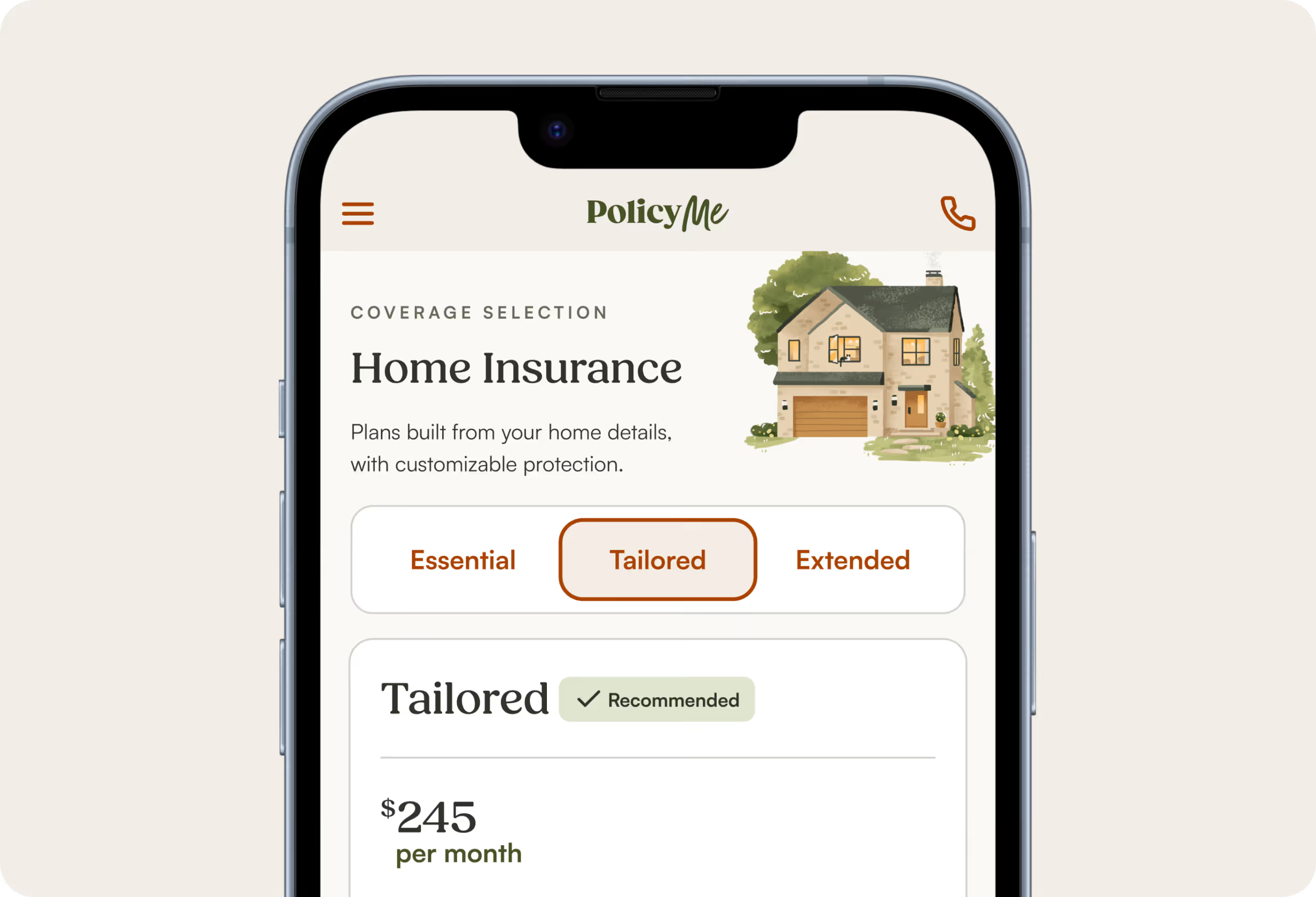

Home insurance quotes for Ontario homeowners

Couple in their 30s, Ottawa

Home type: Detached house

Rebuild value: $680,000

Year built: 2005

Coverage: Comprehensive

Deductible: $1,000 deductible

Claims history: None in the past 5 years

$2,388/year

Annual premium

$199/month

Monthly rate

Single homeowner, GTA

Home type: Detached house

Rebuild value: $900,000

Year built: 2010

Coverage: Comprehensive

Deductible: $1,000 deductible

Claims history: None in the past 5 years

$3,612/year

Annual premium

$301/month

Monthly rate

Couple in their 40s, older home

Home type: Detached house

Home value: $700,000

Year built: 1945

Coverage: Comprehensive

Deductible: $1,000 deductible

Claims history: None in the past 5 years

$2,784/year

Annual premium

$232/month

Monthly rate

Quotes shown are sample estimates based on standardized homeowner profiles and coverage selections. Your actual premium will vary based on your property details, location, and insurer underwriting criteria.

What impacts your home insurance rate?

Rebuilding cost

Questions about your house’s age, construction type, home systems, maintenance, and more help insurance companies calculate the total rebuild cost for your property.

Property characteristics

Details like the size of your home, the number of units, and the structure of the property can influence your insurance rate.

Location

Proximity to fire stations or hydrants, local property crime rates, and regional risks like flooding or wildfires can affect your home’s overall risk level.

Home features and safety systems

Features like alarm systems, connected smoke detectors, and newer electrical or plumbing systems may help reduce risk and lower premiums.

Claims history

Past home insurance claims are a statistical predictor of future claims, which can influence how insurers price your policy.

Coverage selections

Your deductibles, coverage limits, and optional protections impact your premium. Adjusting these options can change the overall cost of your policy.

What’s included in your PolicyMe home insurance quote

When you receive your home insurance quote, you’ll see several important policy details.

You’ll get the opportunity to review all of your coverage options with a licensed advisor, who can answer any questions you have and help you make any necessary adjustments based on your full financial picture.

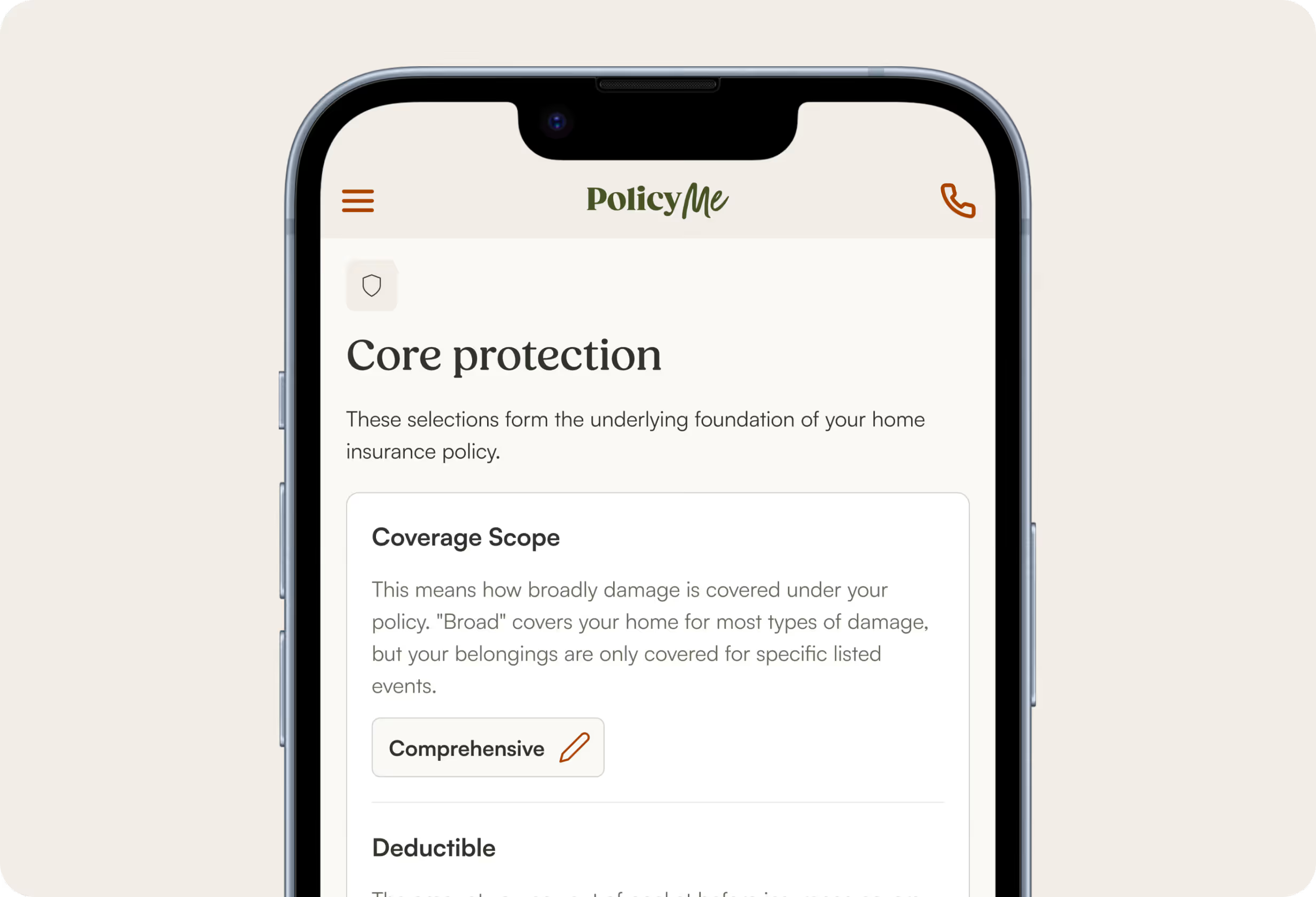

- Coverage scope: This refers to which perils (causes of damage) your policy covers—from basic coverage, which only includes listed perils, to comprehensive coverage, which includes everything except stated exclusions.

- Deductible: This is the amount you’ll pay out of pocket when making a claim. A lower deductible can make claims cheaper, but you’ll pay less for a policy with a deductible of $1,000 or more.

- Limits: You can combine dwelling and contents coverage under one limit, simplifying claims that involve both your home and belongings.

- Dwelling coverage: Your dwelling limit also sets coverage for personal property, other structures, and living expenses. It should be at least 80% of your home’s rebuild cost.

- Personal liability coverage: The starting limit for this type of coverage is usually $1M, but it’s often worth raising it to at least $2M or more depending on your assets.

Personalized quotes from trusted insurers in minutes

Ready to get quick home insurance quotes? With PolicyMe, complete a simple 10-minute online application and instantly see real quotes. No sales pressure, no obligation to buy.

Choose your coverage level

Answer a few questions about you and your home, then select the coverage level you’re comfortable with.

Customize your plan

Once you’ve completed your application, you’ll be able to explore coverage options at different price points.

Review and finalize your quote

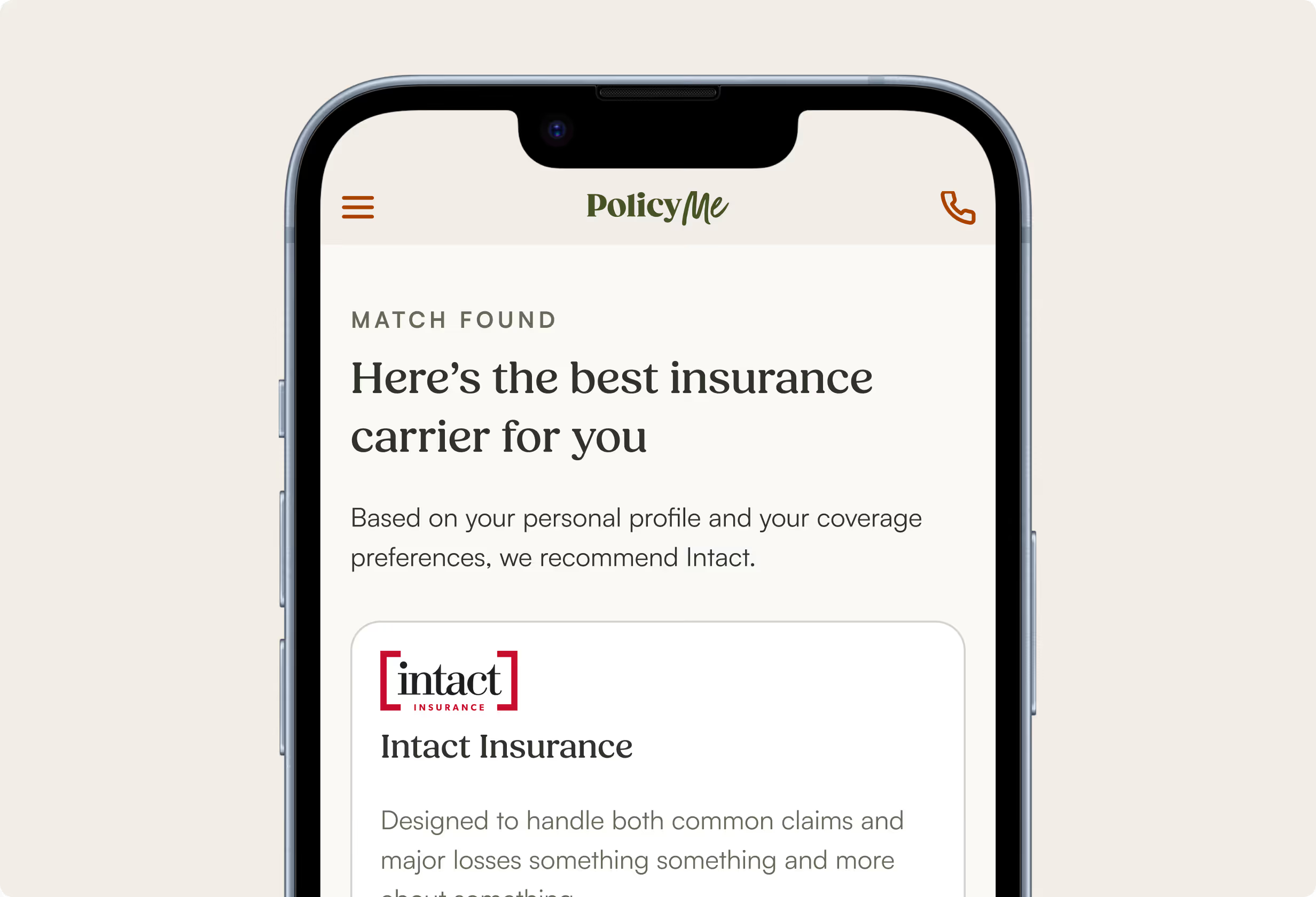

We’ll recommend a trusted insurance carrier based on your profile, though you can review all your options before finalizing your pick.

What you need to get home insurance quotes

Before you request home insurance quotes, it’s worth making sure that you have some documents on hand. You’ll need important information about the property you’re trying to insure, including:

How to save on your home insurance costs

Home insurance is an essential for homeowners, but it’s also a big investment. Smart shopping can help you reduce your annual insurance costs without compromising the financial protection you need.

Bundle your home and auto insurance

Buying car insurance and home insurance from the same company earns you a discount of up to 20%.

Personalize your coverage options

Home insurance policies come with tons of moving parts, so it’s easy to accidentally over- or underinsure. A licensed advisor can help you trim any unnecessary coverage while keeping the key protections you need.

Choose a higher deductible

High deductibles keep your house insurance coverage more affordable—but make sure that you’re still able to realistically pay your deductible in the event of a covered loss.

Compare quotes often

Home insurance shopping isn’t a one-and-done. Re-shopping each year can help ensure you’re always getting the best price for the coverage you need.

FAQ: Home insurance quotes

A home insurance quote is the estimated price of a certain amount of home insurance coverage from a specific insurance provider. It’s not a final price and can change based on updated information when you finalize your purchase.

Home insurance rates are set based on a wide range of variables, and each insurance company analyzes those variables differently. No single insurer has the cheapest rates for every homeowner — the only way to identify the cheapest option for your home is to compare personalized quotes.

Home insurance isn’t required by law for homeowners in Ontario, but mortgage lenders typically require buyers to acquire home insurance in order to finalize their purchase. The same requirements may apply to condo insurance.

On average, Ontario homeowners tend to pay around $800–$1,500 per year for home insurance, with the higher end of the scale representing high-value homes, larger properties, and homeowners in high cost of living areas like the GTA.

Sometimes. Home insurance typically covers water damage due to the sudden and accidental failure of indoor systems, but not overland flooding or water damage caused by outdoor sources like sewer backup. You can purchase overland floor protection and sewer backup coverage as add-ons to your home insurance.

You should review your home insurance policy before you make the first payment and each subsequent year before your renewal date comes around. Check your eligibility for better rates from other insurers and consider whether you need additional coverage.

The most effective way to compare quotes for home insurance online is through a digital insurance broker like PolicyMe. Brokers can access real quotes from multiple insurers, but they don’t work for any insurance company, making them the ideal neutral source for expert-guided comparison.

Vous avez une question à laquelle nous n'avons pas répondu?

Appelez le +1-866-999-7457 du lundi au vendredi, de 9 h à 17 h HNE ou envoyez-nous un courriel. Notre équipe d'experts en assurances est là pour vous aider!