About PolicyMe’s Critical Illness Insurance

Get a tax-free, lump-sum payment if you're diagnosed with one of 44 covered conditions.

Critical illness insurance benefits

A critical illness payout gives you financial breathing room while you heal — whether that means taking time off work, being there for loved ones, or simply not worrying about bills. Here are a few ways your benefits can support your recovery.

Treatment & recovery costs

Key ways people use it

Medications & supplies

Cover medications not included in your benefits, plus medical equipment and supplies.

Extra care & rehab

Pay for additional physiotherapy or rehabilitation, or hire additional in-home nursing care.

Travel for treatment

Cover travel expenses related to treatment (e.g. parking, accommodation, meals), or explore medical treatment options outside Canada.

Accessibility upgrades

Modify your vehicle or home for accessibility.

Personal costs

Key ways people use it

Replace lost income

Replace lost income while you're unable to work.

Reduce debt & monthly pressure

Pay down debt, mortgage, or line of credit.

Support your family

Support unpaid leave for a spouse or family caregiver; fund children’s education or other financial plans.

Household help

Spend this money on cleaning, lawn care, snow removal, meals or taking care of your pets.

Say yes to things you've been putting off

Take a trip, celebrate milestones, or purchase something meaningful.

Professional costs

Key ways people use it

Cover staffing needs

Cover salaries for replacement or additional staff during recovery.

Maintain your pre-diagnosis income level.

Maintain your pre-diagnosis income level.

Adjust how you work

Modify your working hours or duties.

Support business continuity

Pay down business debt or fund a buy-sell agreement.

Professional costs

Key ways people use it

Professional costs

Key ways people use it

Professional costs

Key ways people use it

Critical illness is more common than you think

2 in 5 Canadians will be diagnosed with cancer in their lifetime

According to Canadian Cancer Statistics 2023; the probability of developing cancer for Canadian is 45% for males and 44% for females.

9 in 10 Canadians are at risk for stroke or heart disease – 108,707 strokes annually

Research by the Heart and Stroke Foundation shows that six in 10 Canadians have experienced or had someone close to them experience stroke or heart disease.

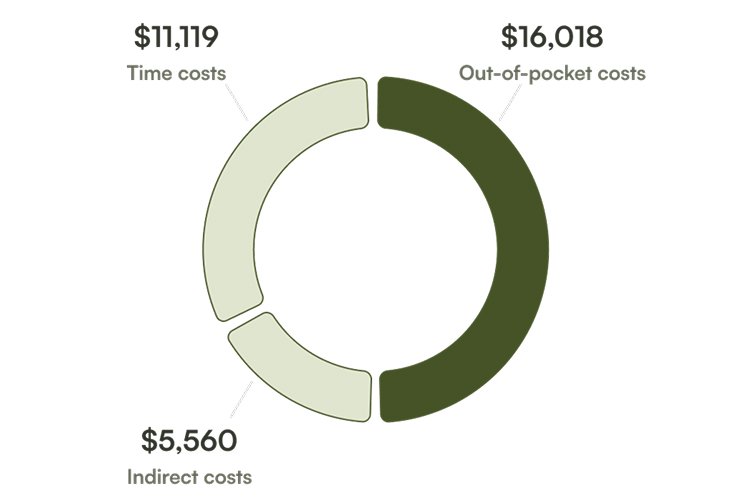

A cancer diagnosis costs Canadians an average of $32,000

People with cancer and their caregivers are expected to incur $16,018 in out-of-pocket costs, $11,119 in time costs, and $5,560 in indirect costs.

Understanding your critical illness insurance payout

Understanding your critical illness insurance payout types

Fully Covered Conditions

Critical Illness Benefits

100% lump-sum payment

If you're diagnosed with any of the 27 fully covered critical illness conditions and have satisfied the waiting period for that condition, you'll receive a lump-sum payment equal to your total coverage amount.

One-Time Payout

Policy ends after a full claim is paid out for any fully covered condition.

Partially Covered Conditions

Early Condition Benefits

15 Early-stage conditions

15% of your policy coverage amount, payout up to $50,000

2 Ablation surgeries

30% of your policy coverage amount, payout up to $100,000Covers Carcinoma In-Situ of the Breast Treated with Total Mastectomy and Early-Stage Prostate Cancer Treated with Radical Prostatectomy.

Important details about early condition benefits

Your full coverage remains intact

Payment of an early condition benefit does not reduce your critical illness benefit amount.

Example

You purchase a policy with $1,000,000 in coverage. You're diagnosed with an early-stage condition that is eligible for a $50,000 payout. If in the following year you're diagnosed with a critical illness that is covered under the plan, your payout will still be the full $1,000,000.

Combined limits for some early cancer conditions

Two early conditions for Early-Stage Breast Cancer are partially covered under your policy. The combined Early Condition Benefit for these two (Early-Stage Breast Cancer and Carcinoma in-Situ (CIS) of the Breast Treated with Total Mastectomy) shall not exceed 30% of your Policy Coverage Amount, up to a maximum of $100,000 for the lifetime of this Policy.

The same logic applies to Early-Stage Prostate Cancer (Early-Stage Prostate Cancer and Early-Stage Prostate Cancer Treated with Radical Prostatectomy).

Example

You have a policy with $500,000 in coverage. You are diagnosed with breast cancer and receive $75,000 for Carcinoma In-Situ of the Breast treated with Total Mastectomy. Later, you are diagnosed with early-stage breast cancer again. Your payout would be $25,000 (the $100,000 combined lifetime limit for breast cancer conditions minus your prior $75,000 payout).

One claim per condition

You can only claim once for each specific early condition. However, some cancer types (breast and prostate) have two related conditions you may be eligible to claim for separately.

Example

You are diagnosed with Bacterial Meningitis and are eligible for payout. If you are later diagnosed with Bacterial Meningitis again, you will not receive another payout.

Maximum of 4 early condition claims

Up to four early condition benefits are available per policy.

Example

If you've received payouts for 4 early conditions and are later diagnosed with a 5th early condition, you will not be eligible for another early condition payout.

Critical illness conditions

This information is for informational purposes only and is not an insurance contract or offer of coverage. It is intended to provide a general overview of the insurance product available to help you make an informed decision. The information presented is subject to change and may differ from the actual policy issued. For full details on the insurance coverage, including terms and conditions, please refer to the final policy contract issued to you or speak with one of our licensed insurance advisors. PolicyMe Life, Critical Illness, and Health & Dental insurance plans are underwritten by Canadian Premier Life Insurance Company of Canada and sales are conducted by PolicyMe Corp. The insurance transaction is between the client and Canadian Premier Life Insurance Company. Securian Canada is the brand name used by Canadian Premier Life Insurance Company to do business in Canada. PolicyMe Corp., doing business as PolicyMe, a licensed Life and Accident & Sickness insurance agency, acts as the administrator and technology provider of PolicyMe Life, Critical Illness and Health & Dental insurance plans on behalf of Securian Canada. PolicyMe is compensated by way of commissions by Securian Canada for sales of insurance. For our full disclosure notices, please visit policyme.com/legal

Product highlights

Receive one lump-sum, tax-free payment if you're diagnosed with any of the covered conditions. Use it to cover medical expenses, replace lost income, pay for childcare, modify your home, or anything else you need during recovery.

Most Canadian insurers only cover 20–30 conditions under critical illness insurance. PolicyMe covers a total of 44:

- 27 critical illnesses fully covered, including cancer, heart attack, and stroke

- 17 early-stage conditions are partially covered, including 9 early-stage cancers

The application takes about 20 minutes to complete. You’ll find out as soon as you submit whether you’re approved or if additional underwriting steps are required. 60% of PolicyMe customers are approved instantly, meaning your coverage can start as early as tomorrow.

24 of the 44 covered conditions have no waiting period, meaning that you can submit a claim as soon as you are diagnosed. This includes all covered cancer conditions.

Choose benefit amounts from $10,000 to $1,000,000 and term lengths from 10-30 years. The term length available to you depends on your age—refer to the table below for details. When you apply, our system will automatically show you the terms you qualify for.

Soins de santé provinciaux* | PolicyMe Garantie Émission Économique | Économique | Classique | Avancé | |

|---|---|---|---|---|---|

Examens dentaires et radiographies pour adultes | |||||

Nettoyages, obturations et extractions dentaires de routine | |||||

Traitements endodontiques (canal) et parodontaux (gencives) | |||||

Services dentaires majeurs (p. ex., couronnes, ponts, prothèses) | |||||

Appareils orthodontiques | |||||

Within the first five years of your policy, you can convert to a longer term without a new underwriting. Your coverage amount stays the same.

This means that:

- A 10-year policy can be converted to a new 15-year, 20-year, 25-year or 30-year policy;

- A 15-year policy can be converted to a new 20-year, 25-year or 30-year policy;

- A 20-year policy can be converted to a new 25-year or 30-year policy; or

- A 25-year policy can be converted to a new 30-year policy.

How your new premium is calculated: Your premium will be based on your age at the time of conversion, using the same health classification from your original policy. The maximum term length available depends on your age at conversion.

If you're diagnosed with a covered condition, a dedicated PolicyMe claim specialist will guide you through the claims process and help you access your benefits.

Documentation & Important Information

Official product name | PolicyMe Critical Illness Insurance |

Insurer | Securian Canada 1400-25 Sheppard Avenue West Toronto, ON, Canada, M2N 6S6 Email: service@canadianpremier.ca Phone (Toll-free): 1-855-883-6176 Website: securiancanada.ca AMF Client Number: 2000829775 AMF Website: autorite.qc.ca |

Distributor | PolicyMe Corp. 199 Bay St. #4000, Toronto, ON M5L 1A9 AMF Client Number: 3002916818 General Inquiries: info@policyme.com Phone: 1-866-999-7457 Website: www.policyme.com |

Issue ages | 18-75 |

Term lengths | 10, 15, 20, 25, 30 |

Coverage amounts | $10,000 to $1,000,000 |

Lives insured | Single (Individual Application) |

Waiting periods | We will only pay a Critical Illness Benefit or Early Condition Benefit if the Waiting Period for that Covered Critical Illness Condition or Covered Early Condition is met. |

When your coverage begins | Your coverage will begin at 12:01 a.m. Standard Time at your address on the later of:

|

When your coverage ends | Your coverage terminates at 12:01 a.m. Standard Time at your address on the earlier of:

We will not pay any other Critical Illness Benefit or Early Condition Benefit for that coverage other than that Critical Illness Benefit or Early Condition Benefit, if payable. |

Premiums | We determine the premium payable by you for the Policy based on the Policy Coverage Amount and term length you selected and your personal information. This information is shown on the coverage details page. We will not increase your premiums unless you make a change to your coverage. All premiums due by the terms of the Policy shall be paid by the Policyholder in Canadian dollars on or prior to the day they are due. You have the choice to pay your premiums annually or monthly.

Payments will be made using the latest payment information that you have authorized the Administrator to charge on a recurring basis. If at any time you wish to stop payments from being charged, you must notify the Administrator at least seven days prior to the day the next premium is due. |

Grace period | Starting after your first premium payment, if a premium is not paid when due, the Policy shall be in default. We will allow a 30-day grace period to pay each premium, during which time the Policy stays in force. A notice will be sent to you at least 15 days prior to the expiration of the grace period. If your premium is not paid before the end of the grace period, the Policy shall automatically terminate. If you are diagnosed with a Covered Critical Illness Condition or Covered Early Condition during the grace period, any of your payable benefits, as applicable, will be reduced by the amount owing to us as of the date of your diagnosis. |

Convertibility | At any point before the fifth anniversary of the Effective Date, you can convert your Policy to a new policy with a longer available term length and the same Policy Coverage Amount, without providing Evidence of Insurability. This means that:

The premium of the new policy will be based on the Policyholder’s age on the birthday closest to the day the new policy becomes in force, and the Premium Class or comparable risk category and underwriting decisions applicable to the original Policy. Any term length conversion will be subject to our rules regarding maximum Issue Ages. |

Cancellation | If you are not satisfied with the Policy, you may cancel it at any time by submitting a Cancellation Request Form to the Administrator.

You will not be charged any cancellation fees or penalties. |

Contestability | You have an obligation to disclose every fact that might influence our decision to issue or reinstate the Policy or influence its terms (a Material Fact). The information we rely on from you includes anything you provide in the Application and any other Evidence of Insurability. We use this information to make our decision and we have the right to contest the validity of the Policy and deny any claim if you misrepresent or fail to disclose a Material Fact. All statements made in your Application and any other Evidence of Insurability will be deemed representations and not warranties. No statement will be used to void the Policy or be used in defense of a claim unless it is contained in your Application or any other Evidence of Insurability. We will not contest the Policy after it has been in force during your lifetime for two years from the Effective Date or the most recent Effective Date of Reinstatement, except for fraud, ineligibility due to misstatement of age, or if you do not pay premiums. |

Standard exclusions | PolicyMe’s Critical Illness Insurance includes the following industry standard terms in it:

It also doesn’t cover conditions due to:

In addition, covered conditions will come with their own condition-specific exclusions that will follow the industry standard. |

Misstatement of date of birth or gender | If your date of birth or gender at birth has been misstated, your Critical Illness Benefit or Early Condition Benefit will be adjusted to the amount that would have been provided for the premiums paid based on your correct age or gender at birth. If you would have been ineligible for coverage had the correct information been provided in your Application at the time coverage became effective, the Policy is void and we will return all of the premiums paid. |

FAQ: Critical illness insurance

Critical illness means being diagnosed with a serious health condition that is often life-threatening.

Insurance companies have different definitions of what a critical illness is and what conditions qualify. Common conditions such as stroke, cancer and heart attack are usually covered in critical illness insurance policies.

The purpose of critical illness insurance is to provide financial support to an individual that has a serious disease or illness. Public health care in Canada may not cover all medications, travel for treatment and homecare. You may also not have an employer group benefit plan or other private coverage to rely on. A critical illness may also mean unpaid time off work and/or additional costs like child care or retrofitting your home.

The lump sum payment you get from critical illness insurance helps to offset these expenses and provide additional financial security during this difficult time.

Illnesses typically covered by critical illness insurance in Canada include heart attack, cancer, paralysis, stroke, organ transplants, Alzheimer's, kidney failure and multiple sclerosis.

Canadian insurers have different definitions of what a critical illness is, but it is essentially a life-threatening illness. Some insurers will only cover serious illnesses like heart attack, while others will also cover early-stage diseases such as early-stage breast cancer.

In Canada, PolicyMe recently introduced the most complete critical illness insurance that covers 44 conditions: full coverage for 27 conditions and partial coverage for 17 conditions. Sun Life and Equitable offer the next best coverage options with 34 conditions covered: full coverage for 26 conditions and partial coverage for 8 conditions.

Curious to see how PolicyMe stacks up against other Canadian critical illness providers? Learn more about the best critical illness insurance in Canada.

Some conditions specify an amount of time that has to pass after you are diagnosed before you qualify for a critical illness payout. This differs by insurance company and by the condition that is covered. Usually, cardiovascular conditions (like heart attacks) are most likely to have a waiting period. That said, most of PolicyMe's covered conditions don't have waiting periods to qualify.

Critical illness insurance typically pays out between $10,000 to $1 million in Canada. You choose your coverage amount when you apply for and sign your critical illness policy. If you want a higher coverage amount, your monthly premium will also be higher, though this rate is also determined by your health status, age and other factors.

Critical illness insurance is always paid out as a single lump-sum amount.

Yes, you can always cancel your critical illness insurance with any Canadian provider.

With PolicyMe, you get a full refund on any premiums you have paid if you cancel within 30 days of the date your critical illness policy became active.

If you cancel after this 30-day period, you will only receive a pro-rated refund of any premiums you have prepaid. You won’t be charged any cancellation fees or penalties.

Yes, you can buy critical illness insurance by itself in Canada. At PolicyMe, you can buy critical illness coverage by itself, you can buy it with term life insurance or you can add it on to existing term life insurance coverage after the fact.

You might still be eligible for critical illness insurance if you have a history of high blood pressure. But you may not be eligible if you’ve had an abnormal ECG or have had heart surgery. You might also be ineligible if you’ve been diagnosed with or have experienced symptoms of:

- Heart attack

- Transient ischemic attack

- Stroke

- Coronary artery disease

Make sure to read your policy carefully to see what other exclusions may apply.

Vous avez une question à laquelle nous n'avons pas répondu?

Appelez le +1-866-999-7457 du lundi au vendredi, de 9 h à 17 h HNE ou envoyez-nous un courriel. Notre équipe d'experts en assurances est là pour vous aider!