Your Guide to Group Life Insurance (2026)

What is group life insurance?

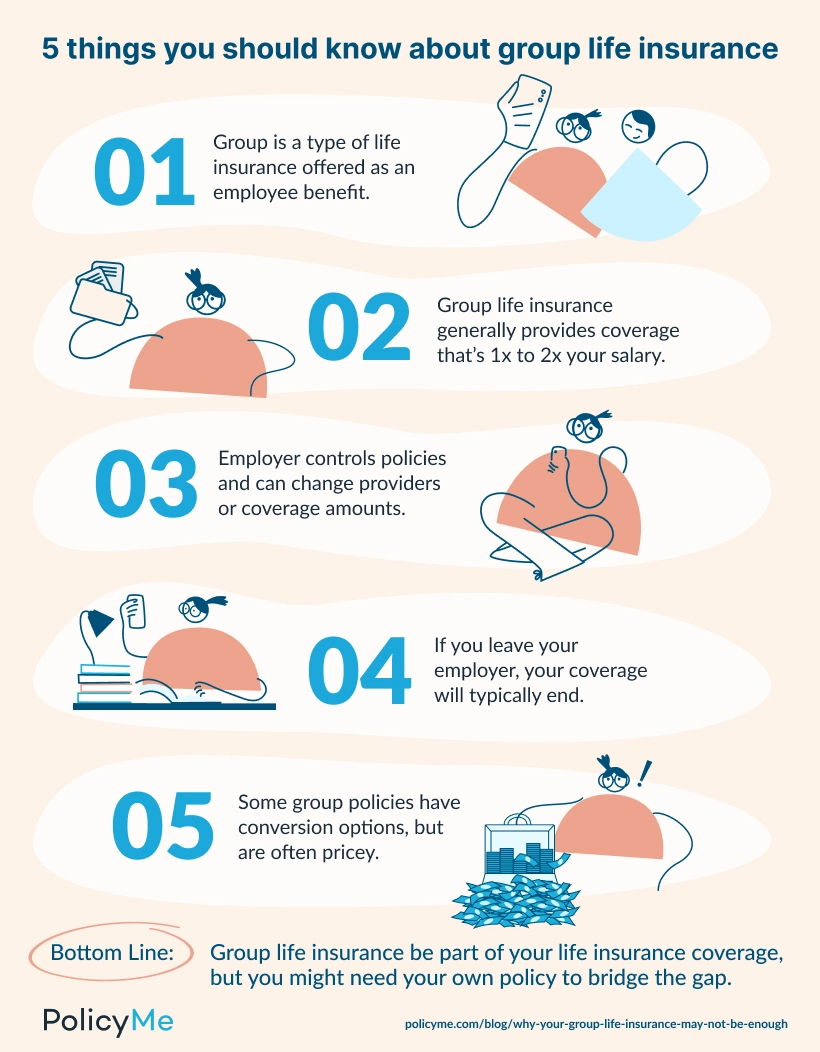

Group life insurance is a type of life insurance coverage that businesses typically offer to employees as part of a benefits package. All employees in the workplace have the same coverage under a single group contract, and enrollment is typically automatic (subject to eligibility).

Just like other types of life insurance, group life insurance coverage provides a non-taxable death benefit to your beneficiaries if you pass away. The death benefit is usually 1–2x your annual salary or a flat amount, which may be too low to support your loved ones fully.

“The policy is risk-assessed and priced for the whole group. And you have coverage as long are a part of said group,” —Michelle Priest, Life Insurance Advisor

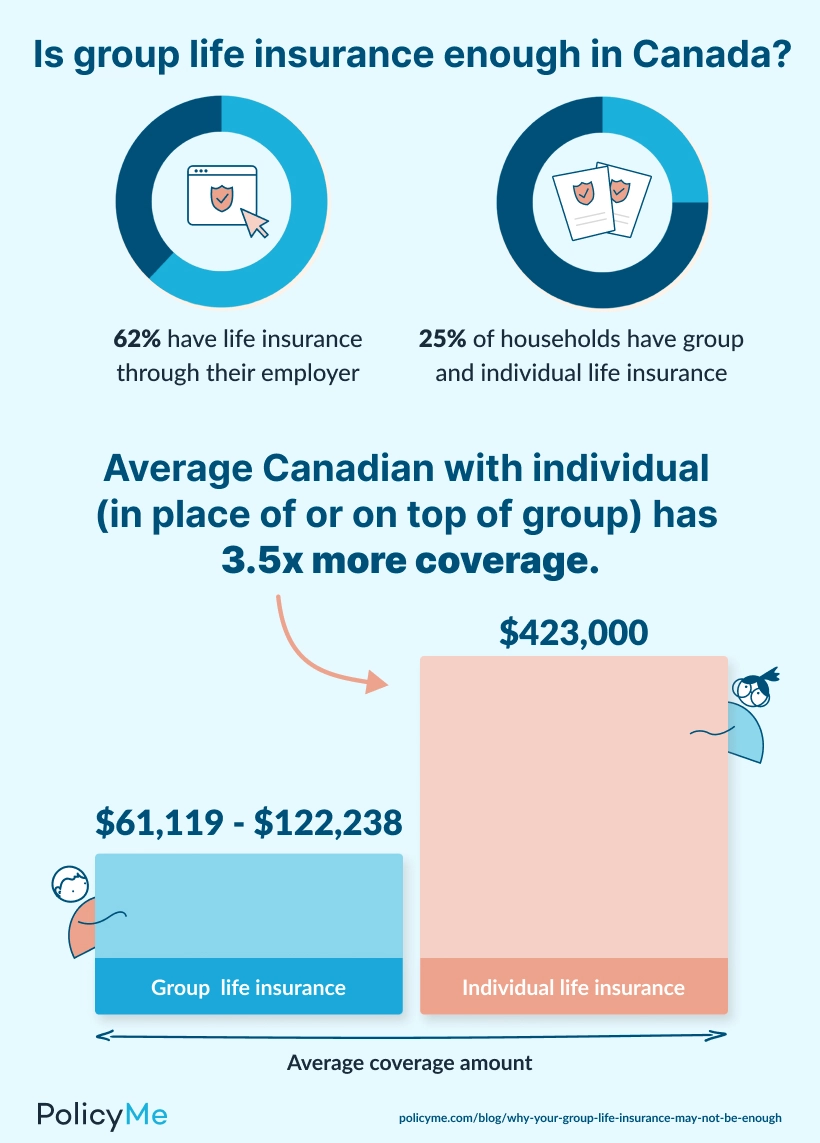

Around 34% of Canadians have group life insurance, but many people opt to purchase an individual life insurance policy, too. Individual policies are unique to you (the policyholder) separate from your employer or workplace. We’ll get into more details about the differences between group and individual life insurance in the sections below.

3 types of group life insurance

The three main types of group life insurance include term, universal, and variable coverage. Most Canadian employers offer term life coverage, which is generally the least expensive option.

Here’s a rundown of each type:

- Group term life insurance: Most employers offer group term insurance (this is probably the one you have!). This is a policy that renews annually and only provides a death benefit within a specified term. It’s the most affordable option of the different types of group life insurance.

- Group universal life insurance: This option allows policyholders to build up cash value in addition to a death benefit. For this reason, it is more expensive than group term life insurance.

- Variable group universal life insurance: Variable group universal life differs from group universal in that it offers investment opportunities alongside the cash value. This means that policyholders can potentially boost their returns with this coverage, but there’s also a risk of policy collapse.

It’s important to keep in mind that you won’t have a choice in the type of life insurance policy provided by your employer or organization. As the owner of the policy, your employer has complete control over the coverage for you and other eligible plan members.

Just need the TL;DR? Here’s a quick explainer video on how group life insurance works:

Is group life insurance enough for you?

The average group life insurance policy is capped at around 1–2x your annual salary, and this is likely not enough coverage to financially support your loved ones.

- Group coverage: 1–2x your annual salary

- Individual policy: 5–10x your annual salary

A group policy payout may offer some short-term relief, but it’s simply not enough for long-term income replacement and financial stability after the loss of a partner. Compared to someone with only a group policy, the average Canadian with an individual plan has approximately 3.5x more coverage.

In the graphic above, we’re using the average Canadian salary of $61,119 and average individual coverage of $423,000 to demonstrate the gap in coverage amounts. To dig deeper into where this gap comes from, think about how much life insurance you need to support your family during a tough time.

Read more: How much life insurance do you need?

“Group life insurance is a nice perk, but it’s something to build on. It’s a good starting point but usually not enough for most families.” —Erik Heidebrecht, Licensed Insurance Advisor

Here are a few example profiles that highlight the shortcomings of group life insurance, plus how an individual policy can fill the gaps:

- Annual salary: $110,000

- Financial obligations: $400,000 mortgage, $10,000 consumer debt

- Group coverage: $110,000

- Is group life insurance enough? No, she would need about $410,000 in coverage to fully protect her family.

- Additional coverage needed? Yes, she would need approximately $300,000 in top-up coverage through an individual policy, which would cost around $14 per month for a 20-year term with PolicyMe.

- Annual salary: $95,000

- Financial obligations: $590,000 mortgage

- Group coverage: $120,000

- Is group life insurance enough? No, he would need about $590,000 in coverage to fully protect his family.

- Additional coverage needed? Yes, he would need approximately $470,000 in top-up coverage through an individual policy, which would cost around $41 per month for a 20-year term with PolicyMe.

Here’s when group life insurance is actually enough

Group life insurance may offer enough coverage for families that could manage on a single income with minimal additional support, or if the amount of coverage aligns with your loved one’s financial needs. For example:

- Your partner has a large income and you've both managed to save a good chunk for retirement

- The lump sum payment offers enough financial support to meet the needs of your dependents

- You don’t have any financial dependents or large debts

- Annual salary: $75,000

- Financial obligations: $4,000 consumer debt, no mortgage

- Dependents: None

- Group coverage: $150,000

- Is group life insurance enough? Yes, it would cover his outstanding debt and leave behind a benefit of $146,000 for his loved ones.

- Additional coverage needed? Not necessary

- Annual salary: $90,000

- Financial obligations: $20,000 student loan, no mortgage

- Dependents: None (spouse is financially independent and earns a high income)

- Group coverage: $200,000

- Is group life insurance enough? Yes, it would cover her student loan debt and give her spouse a cushion to cover rent and final expenses during the transition.

- Additional coverage needed? Only if there’s uncertainty about employment

Remember: You'll no longer have your group policy if you lose or change your job. Even if you don't need a lot of coverage, it’s probably worth considering an individual life insurance policy that's separate from your work.

How much does group life insurance cost?

The cost of group life insurance varies widely depending on the type of plan, coverage amount, employer/group and insurance provider. Premiums are typically per $1,000 unit of coverage (i.e. $0.02 / $1,000), depending on plan type.

Group rates also depend on workplace demographics, including:

- Average age of employees: A company with a higher average age of employees may face higher premiums than a workplace with younger staff.

- Riskiness of the job: Some industries may have a higher risk of claim than others (e.g., policing vs. an office job). These workplaces generally pay higher premiums.

- Group size: Larger groups offer a lower risk of claims across a wider spread of employees, so these groups typically pay less for group life insurance.

- Gender mix: Some insurance companies may assess the gender composition of a group, since life expectancy and risk of illness differ between men and women.

Keep in mind: Each insurance provider offers unique rates, so the amount you pay will depend on the life insurance company and plan sponsor that your workplace chooses.

Some workplaces fully cover the premium payments for group plans, which means you get coverage at no cost. Many employees contribute to the cost of their policies via a deduction from their paycheques. Ask your human resources team if you’re unsure

Group life insurance is typically paired with other employee benefits—like health insurance and/or critical illness coverage—as part of a whole group benefits plan. In this case, you may have one premium that covers all inclusions in your benefits package, or a separate deduction for life insurance.

“You have coverage as long as you meet the requirements and are part of the group. All this means is you are less of a risk to an insurance company when you are part of a group, so the cost can be significantly less,” —Michelle Priest, Life Insurance Advisor

Group life insurance vs. term life insurance

There are a few key differences between individual life insurance and group life insurance, including:

- Who owns the policy

- How much coverage you get

- The cost of the policy

- What happens to the policy if you leave your job

- If a medical questionnaire or medical exam are required

- Whether the policy is a taxable benefit

Group life insurance is a one-size-fits-all product that is negotiated and provided by your employer. This doesn’t mean group life insurance is bad—after all, it provides you with some protection for low or no cost. But group coverage is not usually sufficient for most people.

In contrast, individual life insurance is customizable and based on your financial situation and needs. You decide how much coverage you want and manage the policy yourself.

The bottom line: Group life insurance can offer some financial support, but an individual policy typically provides a higher payout amount that can cover a broad range of financial obligations.

“Group life insurance is a nice perk, but it’s something to build on. It’s a good starting point but usually not enough for most families.” —Erik Heidebrecht, Licensed Insurance Advisor

PolicyMe’s life insurance calculator can help you understand your coverage needs, and our online quote and application process can help you secure an affordable individual term policy in just a few clicks.

What to do if you have group life insurance

If you already have a group life insurance policy, treat it as a starting point, but not a full coverage plan. Ask yourself:

- How much coverage do you and your family need? Meet with your loved ones to discuss numbers. Most people need 5-10x their salary and enough to cover any other debts and future costs as a basic life insurance starting point. → If your group coverage payout doesn’t fully cover your needs, you may need a term policy.

- What are the limits of your group plan? Most group plans are tied to your employment and they’re capped. → If you are concerned about career instability, a term policy can offer peace of mind.

FAQs: Group life insurance

Jaya is a researcher and writer with 3 years of experience in insurance and finance. She writes in-depth content that bridges technical expertise with accessible insights. Her work spans topics such as life insurance, health and dental coverage, car insurance, and financial literacy, helping Canadians make informed decisions about their financial protection. With a background in market research and editorial strategy, she collaborates closely with subject matter experts to ensure accuracy, clarity, and value in every piece.

Jaya is a researcher and writer with 3 years of experience in insurance and finance. She writes in-depth content that bridges technical expertise with accessible insights. Her work spans topics such as life insurance, health and dental coverage, car insurance, and financial literacy, helping Canadians make informed decisions about their financial protection. With a background in market research and editorial strategy, she collaborates closely with subject matter experts to ensure accuracy, clarity, and value in every piece.