Life Insurance After Retirement: What Canadians Need to Know

Do retirees need life insurance?

By retirement, many of life’s biggest expenses—such as raising children and buying a home—are already in the rearview mirror, making life insurance less critical than it is for younger families. But life insurance can be worth it if you have dependents or outstanding debts such as a business loan, car loan, or mortgage.

By providing a tax-free financial safety net for your loved ones and reducing the need to rely on your savings, life insurance for seniors can provide peace of mind during your golden years.

“If you have no mortgage and you have some savings to cover your family's expenses, you might not need life insurance.” — Stephanie Roux, Licensed Life Insurance Advisor

What changes about life insurance after retirement?

Once you retire, your financial situation and responsibilities may change quite a bit—and these changes should influence the way you think about life insurance coverage in retirement.

In retirement, life insurance becomes less about income protection and more about wealth protection and estate planning.

Here are the most common changes in the average Canadian retiree’s finances:

- Your income decreases, so income replacement matters less

- Your debts decrease, so debt payoff matters less

Should I keep, cancel, or buy life insurance after retirement?

Retirees may still need life insurance if they have debt or dependents to support. Not everyone enters retirement debt-free. Your options after retirement include keeping your current policy, adjusting it, or buying a new policy.

If you currently have a life insurance policy, your choices are:

- Keep your policy, even if the payout amount is higher than your coverage needs as a retiree, or

- Adjust your coverage to a lower payout amount if appropriate and enjoy lower premiums, or

- Convert part or all of a term policy to permanent insurance for final expenses or estate needs.

If you’re considering buying a life insurance policy, your choices are:

- Retirees can still qualify for and afford coverage.

- Premiums rise and coverage amounts decrease with age.

- Carefully assess your actual coverage needs as a retiree (final expenses, taxes, wealth transfer).

Be cautious about canceling or decreasing your existing coverage. New insurance for retirees can be very expensive or even unavailable, with premiums and eligibility dependent on your age and health conditions.

Permanent coverage may become more relevant when your financial obligations don't have a clear end date, like supporting a lifelong dependent, covering final expenses, or leaving money behind for loved ones.

You may be able to convert a term policy to a permanent policy with no new medical underwriting. You can also apply for a new guaranteed issue policy with a moderate payout to help with final expenses, remaining debts, or immediate family support.

Which type of life insurance is best for retirees?

Now that you’re retired, you probably have at least one term life insurance policy behind you, and you’re wondering about the advantages of term vs permanent.

Regardless of age, the usual guidelines apply:

Consider term life insurance to cover temporary obligations and permanent life insurance to cover indefinite ones. If your needs fall somewhere in the middle, convertible term life insurance may help you keep options open. Guaranteed issue life insurance may be worth considering if traditional coverage isn’t available to you.

“Generally, between the ages of 50 and 60, you’re coming to the end of your first term and considering whether to get term into retirement age or opt in for a more expensive whole-life plan that’s going to act as final expense coverage whenever you pass away.” — Erik Heidebrecht, Customer Service Manager & Licensed Insurance Advisor

Term life insurance for retirees

Term life insurance lasts from 5-40 years and covers temporary financial obligations. Paying off a car, mortgage, ATV, or motorhome; repaying a business loan; or supporting a young dependent until they’re financially self-sufficient all fall into the term life insurance bucket.

The biggest advantage of term life is that it’s simple, affordable, and renewable. When it runs out, you can either let it renew, shop for another policy, or convert it to permanent coverage (more on that later).

Thanks to its affordability and simplicity, term life insurance is the best choice for the majority of Canadians. It provides financial protection for your family without locking you into a lifelong arrangement you may not need (or be able to afford) by the time you get older.

Permanent life insurance for retirees

Permanent life insurance products last as long as you keep paying premiums, making it the suitable choice for covering indefinite financial obligations. The cost of caring for a disabled dependent for the rest of their life or paying for a large funeral can easily exceed the average Canadian’s post-retirement savings.

Permanent life insurance can make sense when your financial obligations don't have a clear end date. For retirees, that often means covering final expenses, supporting a lifelong dependent, or leaving money behind for loved ones.

Unlike term life insurance, permanent coverage doesn't expire as long as you keep paying premiums.

There are several types of permanent life insurance available in Canada, including term 100, whole life, universal life, and guaranteed issue life insurance.

For most retirees considering permanent coverage, the choice often comes down to:

- Term 100 policy: T100 life insurance is generally more sustainable because it’s more affordable, which helps maintain your family’s financial security in the long run.

- Guaranteed issue: Guaranteed issue provides eligible applicants with lifelong coverage without the usual medical underwriting process. It may be worth considering if health concerns make traditional coverage difficult to qualify for.

Permanent life insurance tends to make the most sense when you're planning for expenses that don't disappear with age, like lifelong dependent care, estate needs, or final expenses.

Converting term to permanent life insurance

Retirees often consider buying permanent coverage to lock in lower life insurance rates and avoid rejection if they develop a medical condition in the future. Convertible term life insurance is a cost-effective alternative for maintaining cheap coverage without closing the door on a permanent policy.

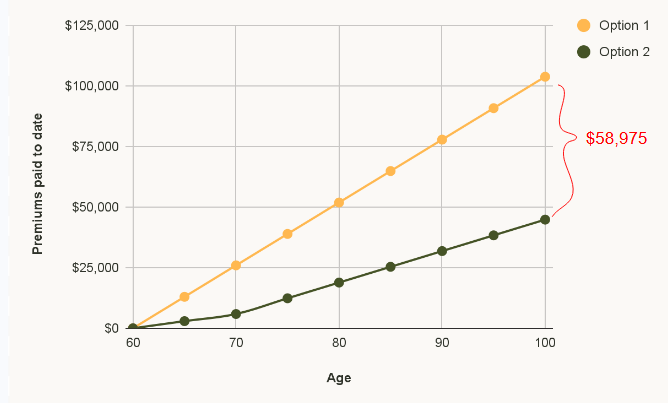

Let’s say you’re a 60-year-old, non-smoking man looking for a policy that’ll provide a $150,000 lump-sum payout. After researching the best life insurance providers in Canada, you’re torn between buying two life insurance options: a term 100 policy or a convertible, 15-year term life insurance plan from PolicyMe.

Option 1: Term 100 life insurance is more expensive, so you take $100,000 in coverage, even though you worry an accident could leave your family members with an unmanageable loan. The cottage is paid off in 10 years, but you don’t want to abandon the equity you’ve built in your policy, which costs $196/month.

Option 2: You buy a 15-year convertible term life insurance policy with $150,000 in coverage, paying $49/month, but health issues at age 70 convince you to invest in permanent coverage. You convert your policy without having to submit proof of insurability, and because the cottage is paid off, you lower your coverage to $25,000, which costs $108/month.

Option 1 leaves you underinsured when it matters most, and overinsured when your finances are vulnerable. Since it costs nearly $200/month, there’s a high chance you’ll cancel your policy and forfeit your investment.

Option 2 is more affordable and tailors your life insurance coverage to each stage of life. Assuming you stop premium payments at age 100, you’ve saved nearly $60,000.

Affordability is a key concern when considering permanent life insurance. If your life insurance premiums become a financial burden, you could lose all the value you’ve built in your policy until that point.

How much life insurance do retirees need?

There’s a simple, three-step process to figure out how much life insurance you need at any age:

- Multiply the annual cost of providing for your beneficiaries by the number of years they require support.

- Add the cost of resolving every outstanding debt.

- Subtract the total value of the savings and assets your family can afford to sell after your passing.

A life insurance calculator helps make the math easier. Our research shows older policyholders typically choose a 15-year term life insurance policy with $100,000 - $250,000 in coverage.

General rules of thumb (like multiplying your annual income by 10-15 times) can be a good starting point, but they risk leaving you over- or underinsured. Going overinsured is especially difficult if you live on a fixed retirement income and dwindling savings.

Life insurance policies with changeable coverage are easier to downsize than to increase. Start at the upper limit of your calculations and downsize later if you have to, but be warned: your premiums may not decrease as much as you like.

How much does life insurance cost in retirement?

Life insurance costs for retirees start at an average of $36/month for a fully underwritten, 10-year term life insurance policy with $50,000 in coverage for a 50-year-old, non-smoking woman. Choosing a permanent policy with the same amount of coverage for the same customer raises the starting price to $103/month.

Longer term lengths and higher coverage amounts result in higher premiums. Your choice of life insurance company matters too. The table below compares the industry average life insurance quotes for non-smokers to those from PolicyMe:

* Table displays the approximate average monthly cost of a 15-year fully underwritten term life insurance policy with $250,000 in coverage for a non-smoking applicant of average health.

** Table displays the cost of a term life insurance policy with the same term length, coverage amount, and underwriting requirements, and for the same type of applicants, averaged across all products contained in our study.

Underwriting is another major factor in life insurance. Fully underwritten policies, which sometimes include a life insurance medical exam, give a more accurate picture of your health and are generally cheaper. No medical life insurance (which includes simplified and guaranteed issue policies) asks few health questions and skips the medical exam, causing insurers to charge higher premiums by assuming you may have pre-existing conditions.

Even for non-smokers, there’s a significant difference between PolicyMe’s fully underwritten life insurance rates and the industry average for no medical life insurance:

* Table displays the approximate average monthly cost of a 15-year fully underwritten term life insurance policy with $250,000 in coverage for non-smokers.

** Table displays the cost of a no-medical term life insurance policy with the same term length and coverage amount, and for the same type of applicants, averaged across all products contained in our study.

FAQ: Life insurance for retirees

Bonnie Stinson is an insurance writer and researcher in Toronto with a decade of experience producing helpful, accurate content for Canadians. They have published resources for some of Canada's most innovative and consumer-trusted companies in the health, legal, and fintech sectors.

Bonnie Stinson is an insurance writer and researcher in Toronto with a decade of experience producing helpful, accurate content for Canadians. They have published resources for some of Canada's most innovative and consumer-trusted companies in the health, legal, and fintech sectors.