Your Quick Guide to Funeral Insurance in Canada

What is funeral insurance?

Funeral insurance is a type of life insurance policy intended to help your loved ones pay for funeral expenses and other end-of-life costs.

It's permanent coverage, meaning it stays active as long as you continue paying your premiums. When the policyholder passes away, the insurance provider pays a lump sum to the beneficiary. While many people use the payout to cover funeral costs, it can generally be used for any purpose, including medical bills, outstanding debts or other expenses.

What is funeral insurance used for?

Funeral insurance is designed to help cover funeral costs and other immediate expenses after you die. For some Canadians, it provides peace of mind that loved ones won't have to pay for these costs out of pocket during an already difficult time.

Coverage amounts are typically much smaller than traditional life insurance policies, often ranging from $5,000 to $25,000. Because of this, funeral insurance is generally best suited for people who only need enough coverage to help with final expenses rather than income replacement, debt repayment or long-term financial support for family members.

If you're eligible for traditional life insurance, you may be able to get more coverage for a similar monthly cost. But for people who have health concerns or have difficulty qualifying for standard coverage, funeral insurance or guaranteed issue life insurance can provide a simple way to leave money behind for loved ones.

Because funeral insurance is designed for people who may not qualify for traditional coverage, premiums are often higher relative to the amount of coverage provided.

For example, a policy with a $10,000 death benefit and a $50 monthly premium would cost:

- $600 per year in premiums

- $9,600 over 16 years

This doesn't mean the policy isn't worthwhile. For many people, the value comes from having coverage when other options may not be available. However, if you're healthy enough to qualify for traditional life insurance, it's worth comparing quotes before deciding on a funeral insurance policy.

Is funeral insurance worth it?

Funeral insurance can be worth it for some Canadians, but it isn't the right choice for everyone.

Because funeral insurance typically offers smaller coverage amounts and higher premiums relative to the payout, it's often best suited for people who want coverage specifically for final expenses or who may have difficulty qualifying for traditional life insurance.

If you're healthy enough to qualify for other types of coverage, you may find better value elsewhere.

Savings: If you have time to build a dedicated emergency fund, setting money aside for final expenses can be a cost-effective option.

Term life insurance: If you qualify, term life insurance can provide significantly more coverage for a lower monthly premium. Your beneficiaries can use the payout to cover funeral costs, outstanding debts, income replacement and other financial needs.

Guaranteed issue life insurance: If health concerns make traditional coverage difficult to get, guaranteed issue life insurance can help ensure your loved ones receive a lump-sum payout when you pass away. While premiums are typically higher than fully underwritten policies, coverage is available without medical exams or health questions.

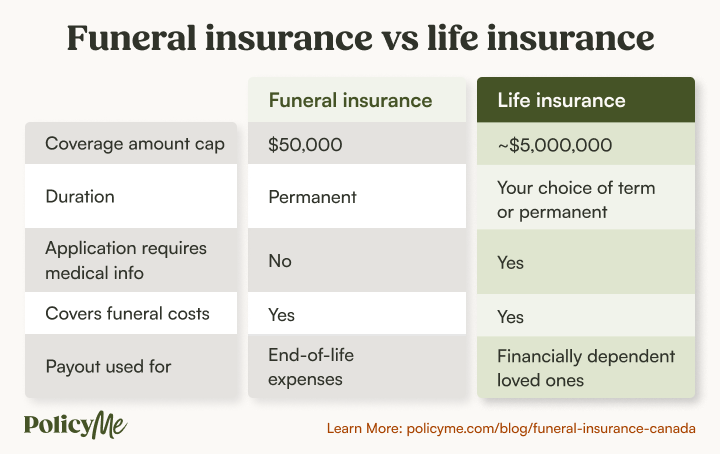

Funeral insurance vs. life insurance

Let's look at a rundown of the differences between funeral insurance and life insurance plans:

Funeral insurance:

- Can be used to pay for end-of-life expenses like funeral costs and final arrangements

- Can take care of caskets, services, and burial/cremation costs

- May relieve your loved ones from the immediate financial burden of your death

Life insurance:

- Provides broader financial protection for your loved ones

- Offers a bigger payout that can be used for anything your family needs, including paying off a mortgage, medical bills, and covering childcare expenses

- Makes the most sense for those with dependents and significant financial responsibilities

The bottom line: Funeral insurance is designed to cover end-of-life expenses, while standard life insurance offers broader financial protection for your loved ones.

Read more: How to find affordable life insurance

Can life insurance cover your funeral expenses?

Yes, life insurance can cover your funeral expenses and anything else your family needs if you pass away.

Depending on the policy, the death benefit amount for traditional life insurance is generally much higher than the payout for funeral insurance. Life insurance payouts provide more comprehensive financial support, covering not just funeral costs but also debts, living expenses, and future needs for your loved ones.

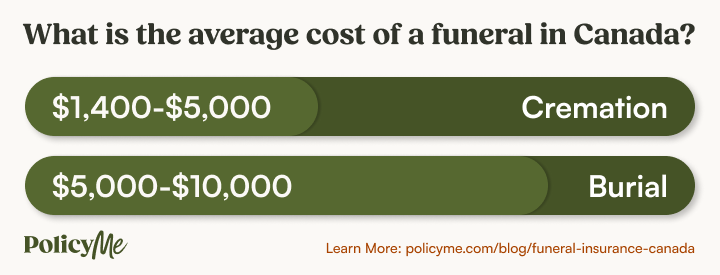

Most life insurance companies offer policies with a death benefit of up to $5 million, though some companies offer even more. The average cost of a funeral is around $8,000, according to data from the National Funeral Directors Association. This leaves your loved ones with a substantial tax-free lump sum to do with as they wish.

Common uses for a life insurance death benefit include:

- Paying off the mortgage

- Setting up a tuition fund

- Loved one taking time off work

- Loved one saving for retirement

What does funeral insurance cover?

Funeral insurance can be used to cover specific costs. The main goal is to help your family cover end-of-life expenses, including:

Pros and cons of funeral insurance

The big appeal of funeral insurance in Canada is peace of mind—that you could qualify for a guaranteed payout with minimal medical requirements. But the drawbacks are major, such as extremely high premiums and limited flexibility.

Types of funeral insurance in Canada

Funeral insurance is not actually a distinct type of policy in Canada, so it’s not accurate to say there are types of funeral insurance. Payouts from any life insurance policy (simplified, guaranteed, or fully underwritten) can be used to cover your final expenses.

“Funeral insurance” is a marketing term that may describe several types of small, permanent policies aimed at helping someone cover end-of-life expenses.

Most policies marketed by insurance providers as “funeral insurance” are permanent no medical policies, of which there are two main types:

- Simplified issue: Minimal health questions, high cost, low coverage

- Guaranteed issue: No health questions, highest cost, lowest coverage

Here’s another way to understand these types of coverage.

- Funeral insurance is almost always a simplified issue or guaranteed issue policy.

- Simplified and guaranteed issue life insurance may be used for funeral costs, but these policies can also provide a moderate amount of final expense coverage and income replacement for anyone who cannot qualify for traditional coverage or who does not wish to answer medical questions.

Each policy has different features, benefits, and eligibility requirements.

What coverage should you consider first?

The first step in thinking about coverage for funeral bills is to estimate the total cost of your end-of-life expenses. Once you know how much coverage you need, you can look for the best possible policy for that amount based on your health and your eligibility.

When I die, how much money is needed? Add up funeral costs for your desired memorial. Consider final expenses for after your passing, like taxes, outstanding debts, and legacy gifts for loved ones. If you have any assets that can help pay for these, subtract that amount.

Right now, what coverage can I qualify for? Start by applying for fully underwritten policies. Even older adults in moderate or poor health should attempt to qualify before considering simplified and guaranteed issue policies.

If health issues truly make you ineligible for standard coverage, then try a no-medical policy from a reputable company. PolicyMe’s guaranteed issue life insurance policy may be a good option for Canadians who cannot get a policy anywhere else but still want permanent coverage from a trusted company with a guaranteed yet modest payout.

FAQ: Final expense insurance for funeral coverage

Bonnie Stinson is an insurance writer and researcher in Toronto with a decade of experience producing helpful, accurate content for Canadians. They have published resources for some of Canada's most innovative and consumer-trusted companies in the health, legal, and fintech sectors.

Bonnie Stinson is an insurance writer and researcher in Toronto with a decade of experience producing helpful, accurate content for Canadians. They have published resources for some of Canada's most innovative and consumer-trusted companies in the health, legal, and fintech sectors.