500 Grand, Gender Gaps, and Gen Z: A Snapshot of Term Life Insurance in Canada

Life insurance is a personal decision, but that doesn’t stop us from wondering how we compare to the norm. How much life insurance coverage do people usually buy? Who are the most common beneficiaries? Is it normal to mention anxiety on your term life application?

To answer these questions and more, PolicyMe analyzed over 18,000 customer interactions between October 1 and December 31, 2025. “Canadian Term Life Insurance: A Market Snapshot” provides a data-driven look at how Canadians are protecting their families, and reveals four surprising facts about the state of the industry.

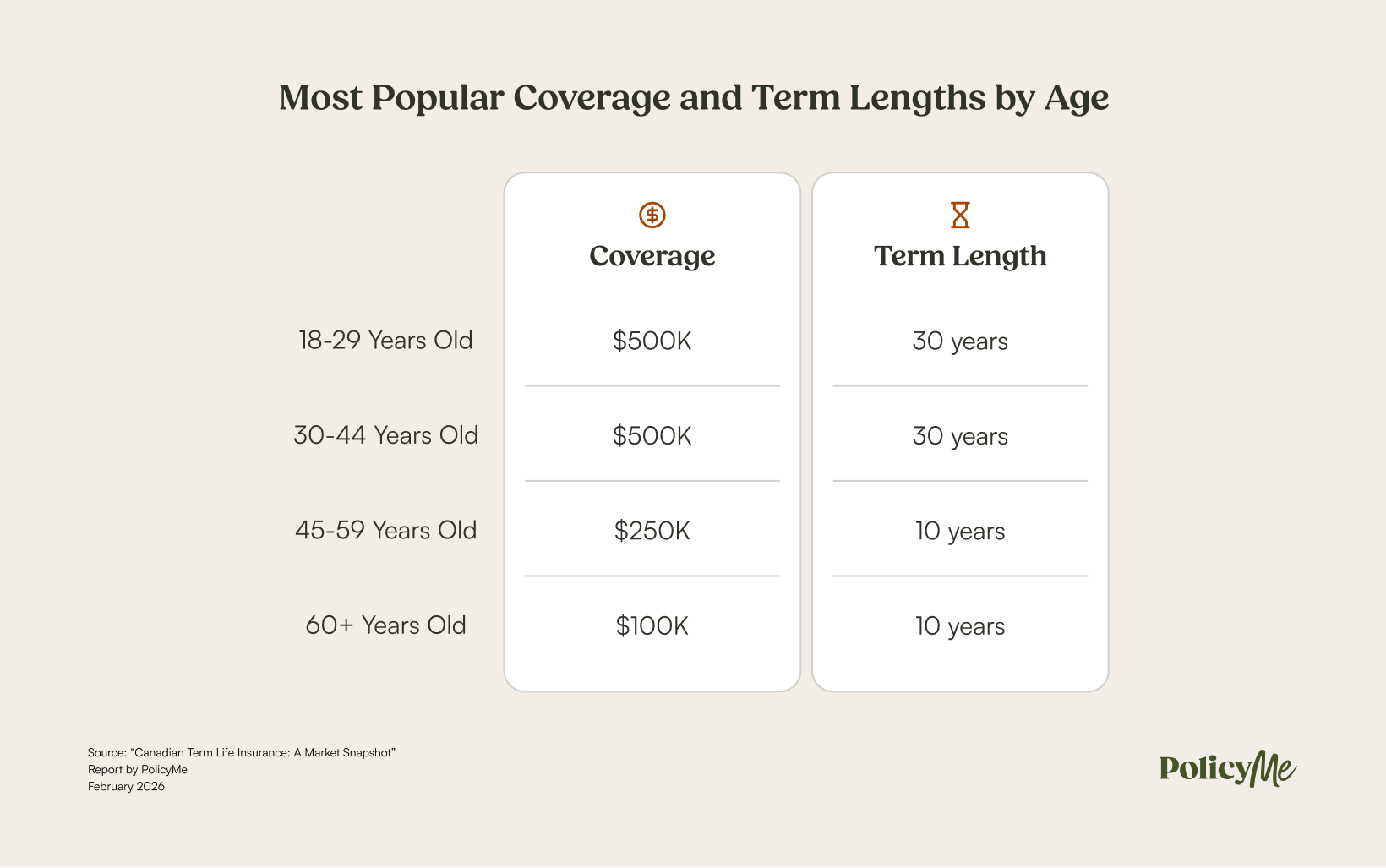

Half a million in coverage wins the popular vote

Regardless of age or income, $500,000 was the most commonly selected term life insurance coverage in Canada. Canadians also gravitated toward 30-year terms, particularly younger adults aged 18 to 44, who selected terms twice as long as those aged 45 to 59.

“There’s no one-size-fits-all number when it comes to life insurance,” explains Andrew Ostro, PolicyMe’s CEO. “The popularity of $500,000 suggests Canadians are seeking meaningful protection without stretching their budgets. Coverage and term length naturally shift as financial obligations grow or shrink over time.”

In other words, life insurance decisions closely mirror life stages. Larger policies and longer terms align with years marked by mortgages and dependent children, while smaller policies and shorter terms become more common as financial obligations ease.

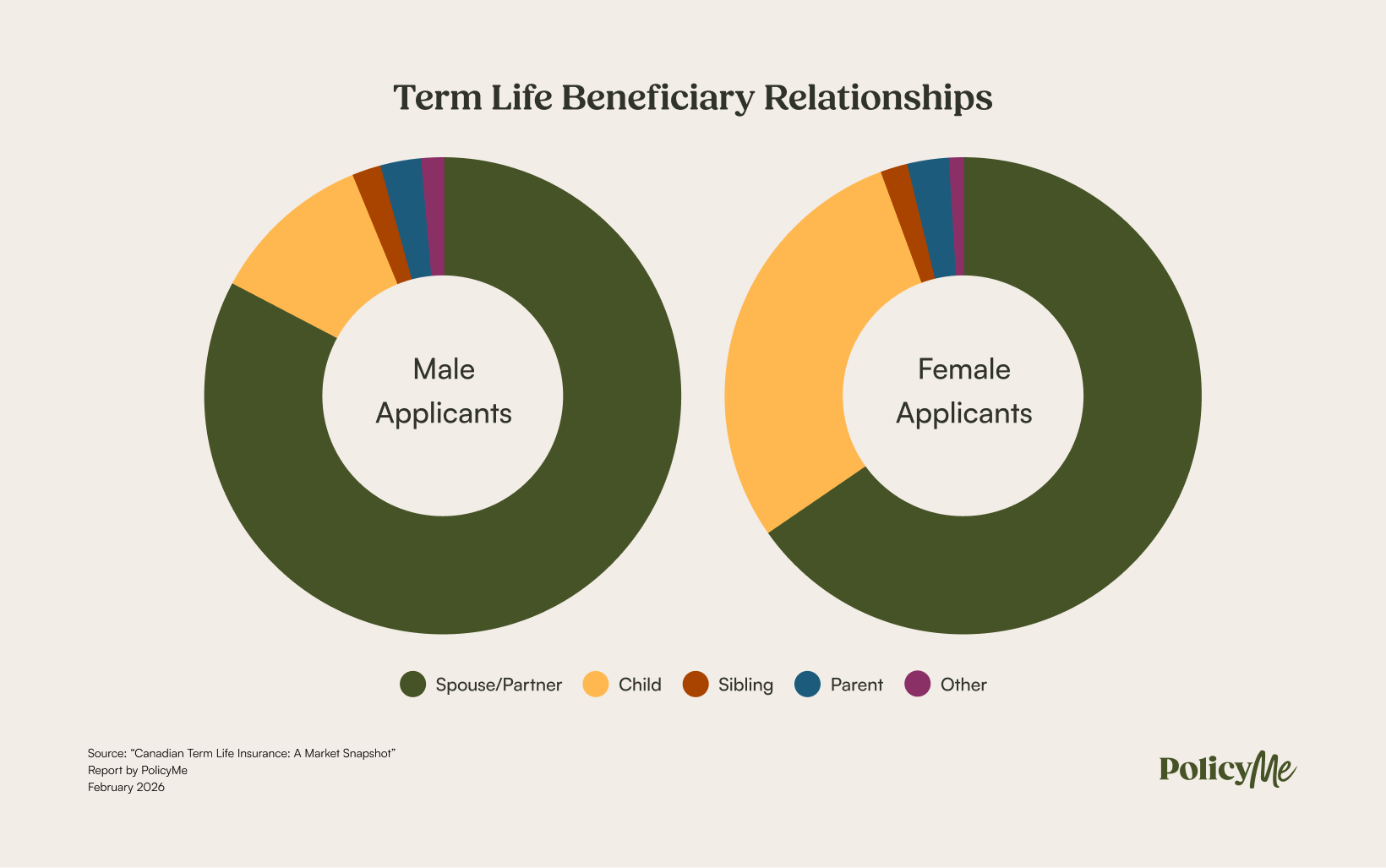

Women insure children, men insure partners

Spouses and partners dominated as insurance beneficiaries, with nearly three-quarters of Canadians naming a spouse or partner. Men named their spouse or partner as a term life insurance beneficiary 83% of the time, compared to 66% of women, who were more than twice as likely to include children in their policy.

The gender gap suggests financial decisions may be influenced by family roles and responsibilities. While the data highlights clear patterns, further research would help clarify what factors most strongly influence these choices, particularly as household dynamics continue to evolve across generations.

Mental health tops the charts for young Canadians

Among the Canadians who disclosed health information as part of the application process, a little over half reported being diagnosed with, suffering from, or getting treatment for at least one medical condition. More than one-third of customers aged 18-29 indicated a mental health-related condition, compared to just under 4% of those aged 60 and over.

As more Canadians openly discuss and disclose their struggles with mental health, generational risk profiles will continue to change, prompting the life insurance industry to continue adapting alongside them.

Gen Z drinks less, but smokes more

Young Canadians report very little daily alcohol consumption, with just 1% of customers aged 18-29 reporting one or more alcoholic drinks per day in the past 12 months. By contrast, Gen Z customers reported consuming nicotine and cannabis at higher rates than any other generation before them–sometimes nearly three times more than their Baby Boomer counterparts!

What young Canadians might not realize is that underwriters typically treat any form of nicotine consumption similarly to smoking, which can significantly affect their life insurance premiums. The use of cigarettes, vapes, and chewing tobacco can all raise your life insurance rates, regardless of perceived differences in “healthiness” or nicotine content.

If you’re young and applying for life insurance for the first time, it’s worth researching topics like how marijuana can impact life insurance. Reading up on the best life insurance for smokers can help you find better rates and make more informed financial decisions.

What our research means for Canadians

Life insurance decisions are shaped by life itself, reflecting competing financial obligations like mortgages and children, alongside changing health realities and lifestyle habits.

PolicyMe’s snapshot of the term life insurance market reveals how closely these factors are interconnected and how nuanced insurance coverage decisions can be. Differences emerged across genders and generations, in some cases highlighting a gap between evolving risk profiles and current underwriting practices.

The findings in “Canadian Term Life Insurance: A Market Snapshot” merely underscore a broader truth: Canadians’ lives are continually changing.

“Life insurance should evolve alongside the people it’s designed to protect. By combining data insights with technology, we can work to design coverage that fits modern Canadians’ lives, not the other way around.” –Andrew Ostro, PolicyMe CEO

Life can be unpredictable, but your insurance doesn’t have to be. PolicyMe offers a streamlined path to assessing your coverage needs, getting a quote, and securing financial protection for the people who depend on you.

Whether you’re purchasing your first policy or reviewing existing coverage, a time commitment of less than 20 minutes today could lead you to lasting peace of mind.

Methodology

These are the findings of an analysis of over 18,000 customer interactions with PolicyMe completed between October 1 - December 31, 2025. Responses were recorded in English and French by Canadians aged 18 and over.

Customer data is self-reported and not subject to independent verification.

PolicyMe takes data privacy seriously. All customer responses have been anonymized. To further protect client confidentiality, findings are presented only where sample sizes meet minimum reporting thresholds, and no individual-level data is disclosed. You can read more about our privacy policy here.

Jasmine specializes in converting complex insurance data into actionable guidance. Her background includes auto, life, and health insurance and financial planning. Lately, she’s leveraging AI to extract insights from the numbers and help Canadians make better decisions.

Jasmine specializes in converting complex insurance data into actionable guidance. Her background includes auto, life, and health insurance and financial planning. Lately, she’s leveraging AI to extract insights from the numbers and help Canadians make better decisions.