Life Insurance Starts With A Mortgage For Many Canadians: Data Report

Why mortgages & life insurance go hand in hand

A mortgage is one of the most significant commitments in modern adult life because it creates an immediate, measurable financial risk, one that isn’t necessarily confined to the homeowner. Even if the primary earner passes away, their debt persists, potentially leaving family and dependents with a financial obligation they can’t meet.

This is why most life insurance assessments start by asking if you have a mortgage. A 25-year term life insurance policy is a natural fit for a 25-year mortgage, and can provide enough coverage to keep the family home, send the kids to school, and more if you pass away.

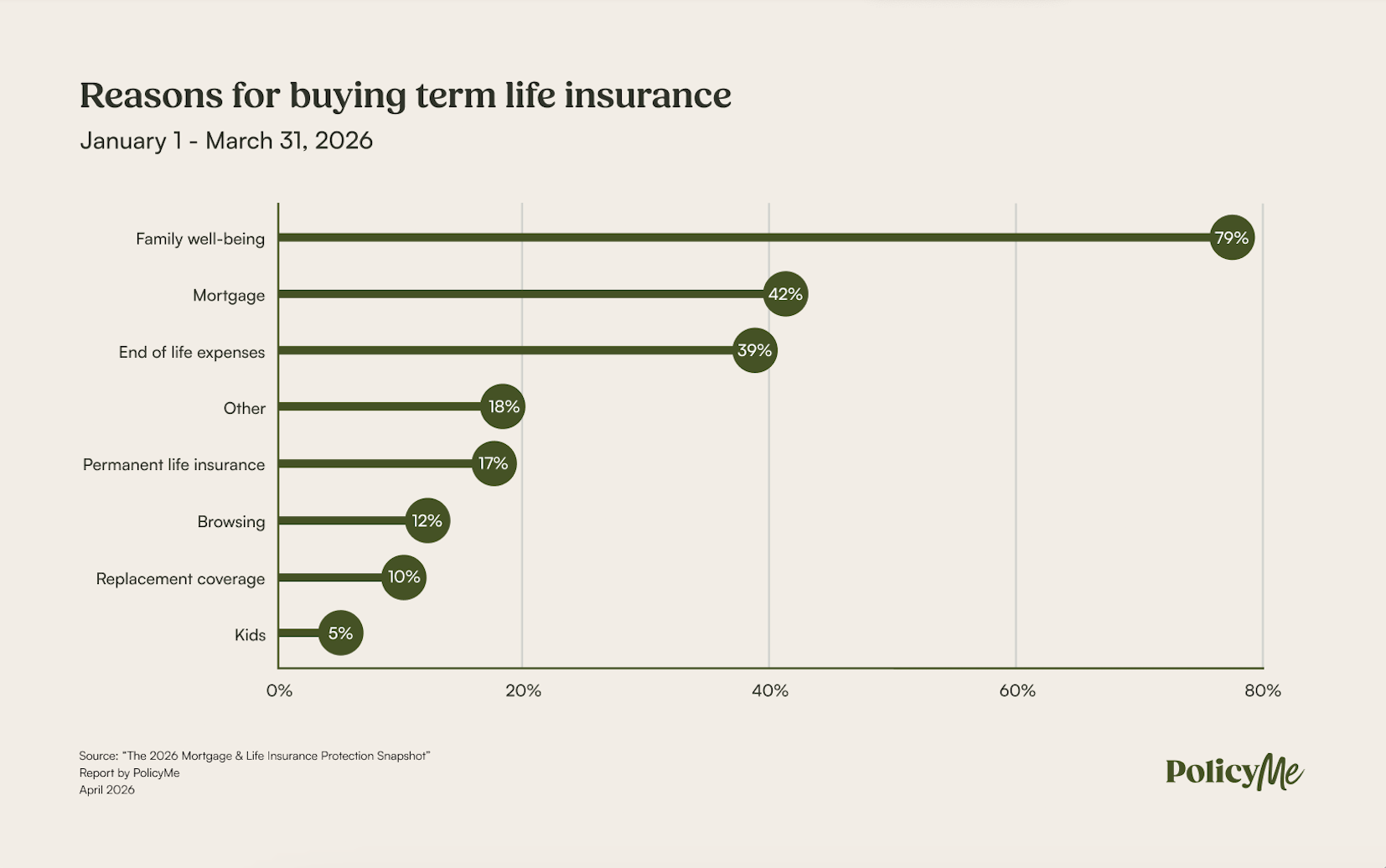

PolicyMe’s latest data confirms this behaviour at scale. In early 2026, 42.3% of applicants cited “mortgage” among their top reasons for buying term life insurance, second only to “family well-being” (79.2%). The two may be one and the same for many Canadians, an urge to protect the family home from the financial fallout of an unlikely but devastating event.

Mortgage buyers choose significantly higher coverage amounts

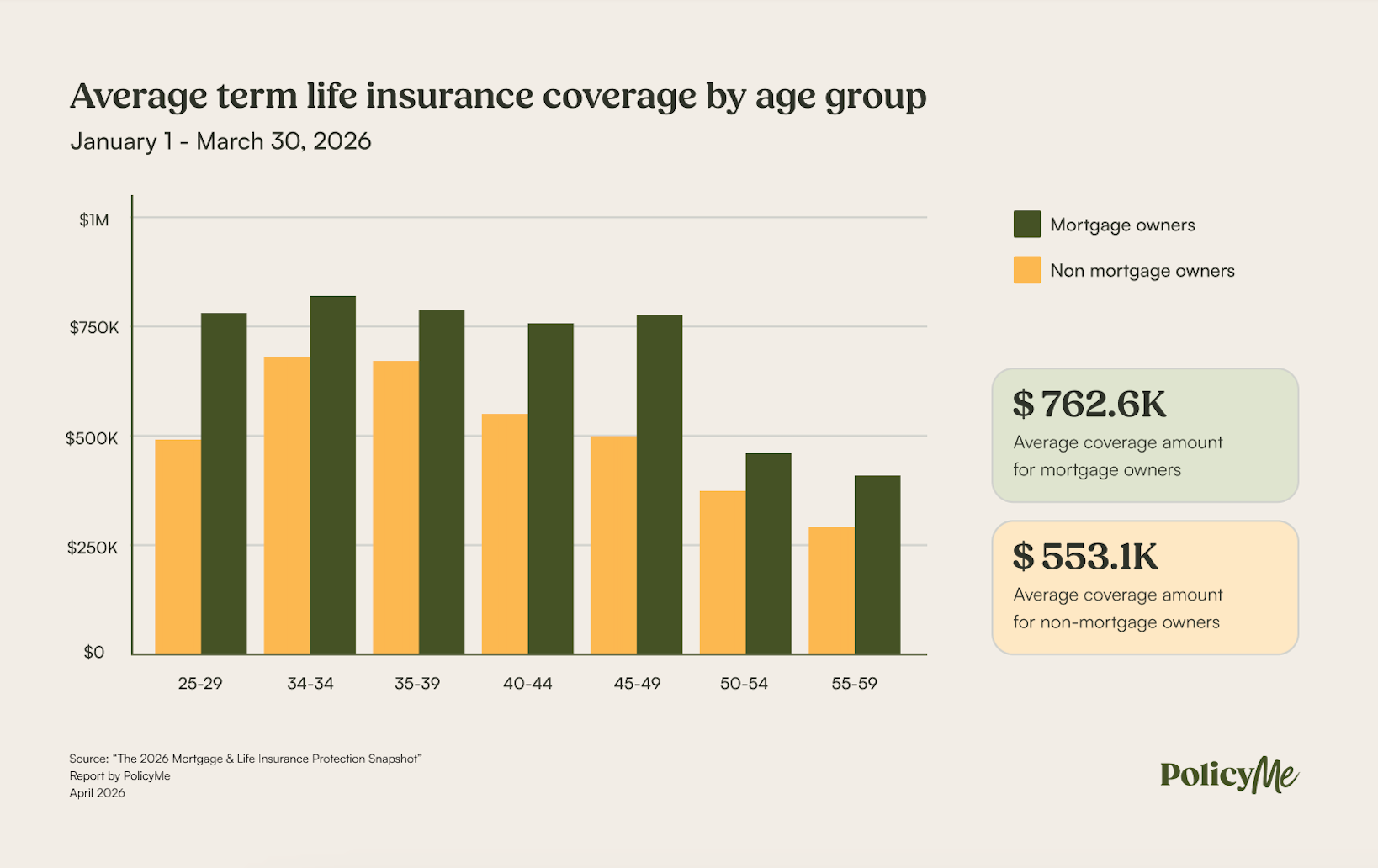

Unsurprisingly, Canadians with a mortgage tend to purchase much more coverage than those without. According to PolicyMe data, mortgage holders selected an average of $762,660 in coverage compared to $553,124 for non-mortgage buyers, a staggering 37.9% difference. Laying aside averages, the most popular coverage amount for homeowners was an even $1 million, compared to $500,000 for non-homeowners.

Given the cost of modern housing, you might expect an even wider gap, but coverage has always been about more than outstanding debt. It’s about the full picture of life after loss and the realities of ongoing living expenses, childcare, income replacement, and more. Regardless of homeownership, when Canadians choose their life insurance coverage, they think about more than just their creditors.

Mortgage-related applications are more likely to be joint. 44.1% of mortgage holders applied with a partner, versus 36.2% of non-mortgage buyers. When debt is shared, so is the decision to protect against it.

What the right coverage amount actually looks like

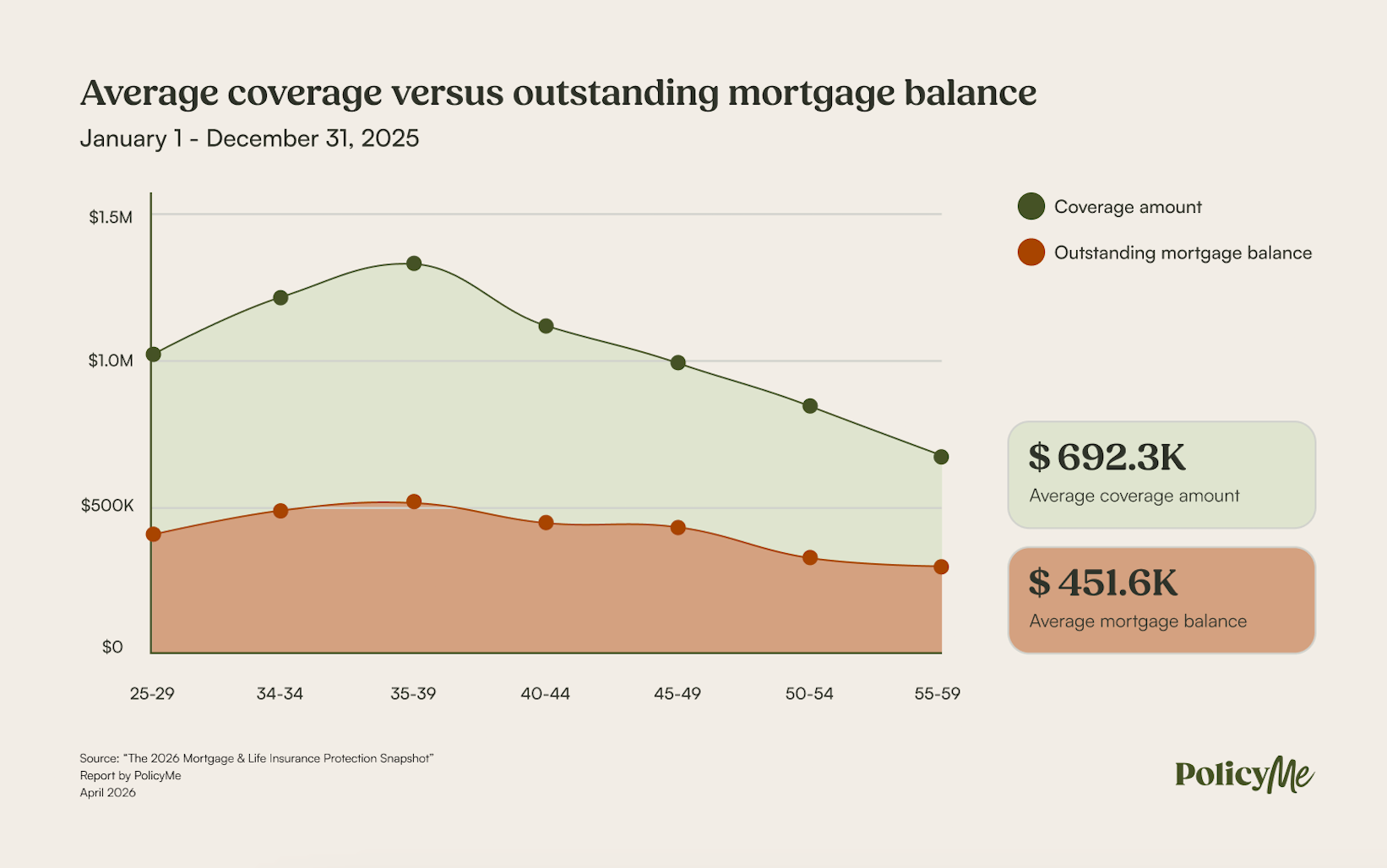

A common question is whether you should buy coverage equal to your mortgage balance. The short answer: probably not.

Among PolicyMe customers with a mortgage, the average outstanding mortgage balance was $451,681 in 2025. The average coverage amount selected during the same period was $692,335, which is 53.3% more than the average balance. That gap reflects what we see consistently: people are buying life insurance to protect their family's financial stability, not just to pay off one debt. A policy that covers only the mortgage leaves income replacement, living expenses, and other obligations unaddressed.

Homeownership happening later, and coverage is shifting with it

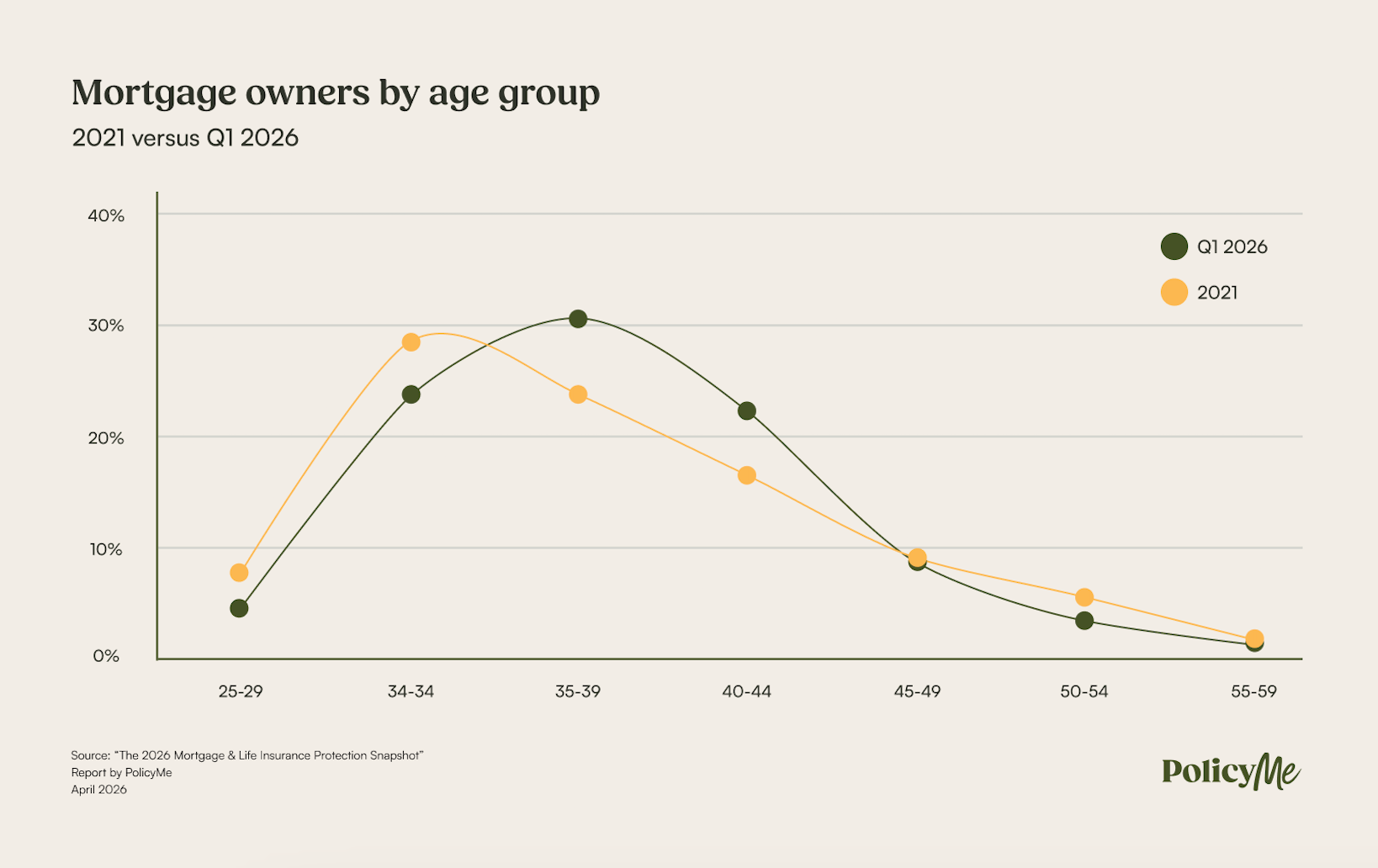

Across all ages, Canadian term life insurance buyers with a mortgage earn roughly 30% (29.7%) more than those without, reporting a yearly income of about $109,500 (versus $84,500). Most mortgage holders in PolicyMe’s data pool, fall within the 30 to 44 age range (77.9%), revealing that owning a home is now more common for middle-aged Canadians, rather than young adults.

This has shifted over time. In 2021, the largest group of mortgage holding customers was between the ages of 30 to 34 (28.9%), followed by 35 to 39 (24.2%) and 40 to 44 (17.1%). By 2026, the peak has moved into the 35 to 39 range (30.9%), signalling that, to no surprise, both homeownership and life insurance decisions are happening later in life. Those aged 30-44 also earn an average 20.4% more in income compared to their non-mortgage peers ($112K vs $93K in income, respectively).

Young homeowners take on more risk (and buy more life insurance)

Canadians aged 25 to 29 request 59.9% more coverage than non-homeowners their age, averaging $783,824 versus $490,190. That gap reflects a mix of high debt and low savings early in life. As a result, many younger buyers are locking in more protection upfront because their financial exposure is significantly higher.

By the early to late 30s, the gap begins to close. Non-mortgage holders in this cohort accumulate more reasons to buy term life insurance, including young dependents, non-mortgage debts, and higher incomes that need to be replaced. Coverage for both homeowners and non-homeowners peaks around ages 30-34 before declining steadily, with one exception.

The second largest coverage gap manifests in the 45-49 age group, where homeowners purchase an average of 55.0% more coverage than non-homeowners ($780,417 versus $503,313). The renewed interest in a high amount of coverage potentially stems from delayed homeownership, the purchase of another property, refinancing, or taking out a second mortgage.

Coverage amounts begin to decline and the gap between homeowners and non-homeowners narrows considerably. Mortgages amortize, kids become financially independent, and financial obligations decrease. Regardless of homeownership status, midlife brings greater assets, greater savings, and a reduced need for coverage.

Mortgage life vs. term life: what’s the difference?

Although homeownership is what prompts many Canadians to start thinking about life insurance, most end up choosing coverage that goes well beyond the mortgage. This versatility is perhaps why 80% of Canadians with term life insurance feel confident about their family’s financial future.

“What we’re seeing is that life insurance decisions are less about a single obligation and more about protecting overall financial stability. The mortgage may be the starting point, but it’s rarely the full picture, since Canadians are also thinking about day-to-day living expenses, household responsibilities, and their long-term financial security. That’s the key difference between regular mortgage protection insurance and term life – its flexibility allows you to protect your overall family financial wellbeing, instead of only covering a single expense.” — Andrew Ostro, CEO of PolicyMe

Unlike mortgage life insurance, term life insurance provides a payout in the amount you choose, which your beneficiaries can use for anything. Plus, the value of your policy doesn’t decrease with your mortgage balance, even as your premiums stay level.

Despite providing a higher, customizable payout, term life insurance often costs 2–3x less than mortgage life insurance. For example, at PolicyMe, a 30-year-old non-smoking woman can get $1M in coverage for only $48.56 per month with a 25-year term, plus 10% off the first year if she applies with a partner.

Because, as the data shows, life insurance isn’t just about debt. It’s about the security and support your family relies on.

Methodology

These are the findings of an analysis of over 1,450 customer interactions with PolicyMe completed between January 1 and March 31, 2026; over 800 interactions completed between January 1 and December 31, 2025; and over 190 interactions completed between January 1 and December 31, 2021. Responses were recorded in English and French by Canadians aged 18 and over.

Customer data is self-reported and not subject to independent verification.

PolicyMe takes data privacy seriously. All customer responses have been anonymized. To further protect client confidentiality, findings are presented only where sample sizes meet minimum reporting thresholds, and no individual-level data is disclosed. Read more in our privacy policy.

Jasmine specializes in converting complex insurance data into actionable guidance. Her background includes auto, life, and health insurance and financial planning. Lately, she’s leveraging AI to extract insights from the numbers and help Canadians make better decisions.

Jasmine specializes in converting complex insurance data into actionable guidance. Her background includes auto, life, and health insurance and financial planning. Lately, she’s leveraging AI to extract insights from the numbers and help Canadians make better decisions.